1. 85% because its commercial

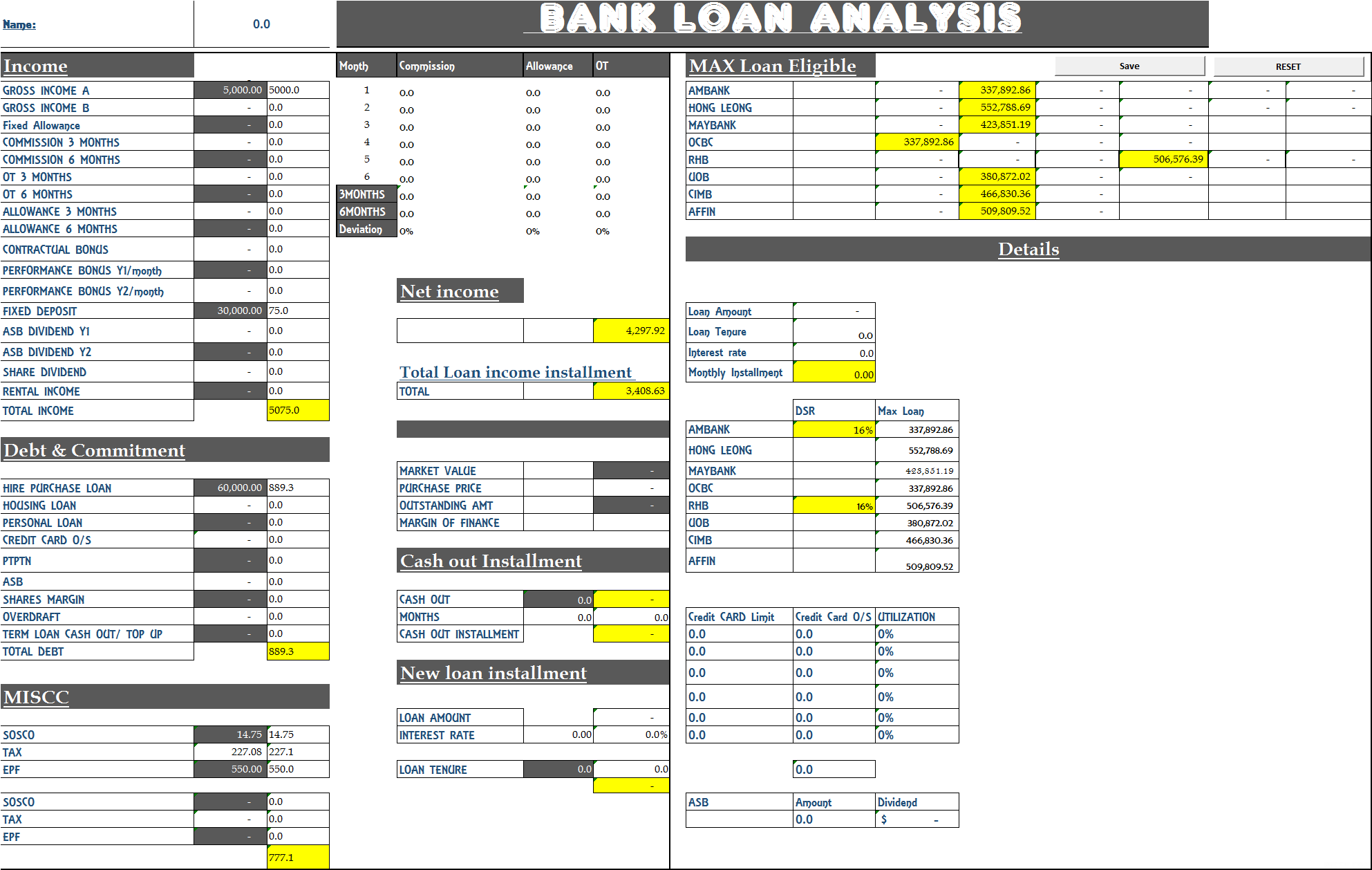

2. Loan amount is based on 85% of the SPA price.

3. You can refinance it for 85% margin subject to your Commitment/Income.

Will need to see ur documents to see if it's advisable to do so since refinancing cashout is calculated within 10 years.

Full flexi

1. Requires current account

2. Monthly fee

3. Prepayment deposit in current account directly reduces principal loan amount thus reduces interest incurred

4. Don't need to notify bank for prepayments

5. No withdrawal fees for prepayment

Semi flexi

1. Savings account will do

2. No monthly fees

3. You may need to notify bank for prepayment / you can also manually transfer prepayment to the loan account without having to notify the bank. Subject to the bank tnc

4. Some banks may need you to notify them

5. Rm10 to 50 for withdrawal fees subject to the bank tnc

Some islamic loan do not impose lock in period so if you intend to settle the loan fast then Islamic loan, otherwise, either 1 is fine.

Opting a higher cashout would mean you need to pay more monthly thus will affect your future loan, you can however use the extra cash out as a downpayment for the new property so you don't have to borrow so much to balance it back.

Normally if you want to cancel your purchase, why would you want to retain the booking fees ? unless you are buying another similar unit with the agent/developer ?

Yeah you can do so, just bear in mind that you will need to pay for a loan agreement since you are transferring to another bank.

I did some google but still a bit confuse about the cost involved for me to do refinance.

I have read some of the previous post found that there is ZMC offer by standard chartered.

But not sure is there any tnc.

Apr 21 2016, 01:23 PM

Apr 21 2016, 01:23 PM

Quote

Quote

0.5934sec

0.5934sec

0.65

0.65

7 queries

7 queries

GZIP Disabled

GZIP Disabled