QUOTE(LNYC @ Jul 18 2016, 09:18 PM)

did u get confuse over my question??

Previously i ask what is the cost for adding another owner in spa..not involving any money transaction here...just transfer of ownership.

of course head small, wear small hat enough lar...too big of the hat very heavy ah~~~

Dear LNYC,

1. If your property now in unencumberance (no mortgage loan) Then you can just transfer or add the ownership via lawyer. Just paying stampduty and other miscc fees, you can alter the ownership.

2. If your property is encumberance( which is with mortgage loan), to alter the SPA ownership, you would need to undergo refinance with the bank or to another bank, it's like new loan. That's the process when the property is with new loan.

So the fees will be as stated before.

Do consider well whether altering the SPA name options

CHeers

QUOTE(cocopuffs @ Jul 19 2016, 01:27 AM)

Is it advisable to ask banker to complete property valuation before I sign offer letter and spa?

What are the costs to bear if valuation done later and valuer give lower value?

Dear,

1. Valuation, usually broker will get valuation from various valuer before submitting the loan to any banks, because loan process needs to have a verified valuation from the bank panel, so that they can only proceed with the loan.

2. After the loan has been accepted, you will sign letter offer. Lawyer will have you sign letter of agreement and SPA if it is ready, and in between the valuer will do a site visit on your property.

3. Broker must be professionla in terms of valuation, as it will affect the clients loan process. Professional consultant will get valuation with valuer with black and white proof, so that anything happen at least they have the evidnce backing that valuer has given such amount. Find a good consultant to guide you will do.

Cheers

QUOTE(Kilohertz @ Jul 19 2016, 11:09 AM)

When you mentioned Title of the property? Do you mean strata title? The property I'm looking at just completed 2 years ago, I'm not sure if the strata title has been issued yet. I would need to check with the agent but what if it's not available?

Dear,

1. if the title has not been transfered yet, you won't need to provide such document to process the loan.

Cheers

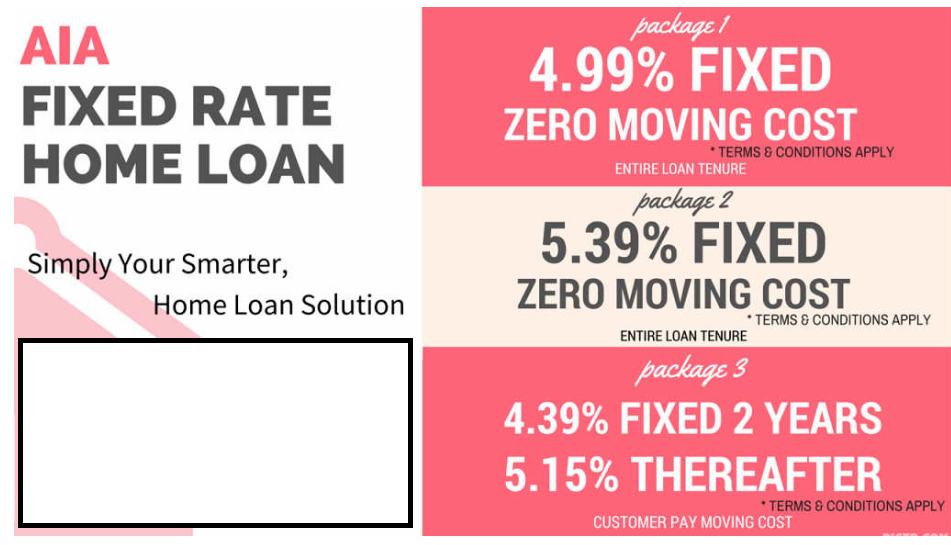

QUOTE(homeSeek @ Jul 19 2016, 12:37 PM)

Recently I made a booking to purchase a property, then I received offers from 3 banks.

CIMB rate is 3.9 (base) + 0.45 (spread) = 4.35, 3-yr locked in.

Maybank rate is 3.0 (base) + 1.2 (spread) = 4.20, 5-yr locked in.

RHB rate is 3.9 (base) + 0.5 (spread) = 4.40, 3-yr locked in.

They offer many different kinds of loan packages, some of them need to open current account, which need a monthly maintenance fee RM10++, some no need but have to keep a min RM1000 balance. For those packages that no need current account, bank will charge a RM25~RM30 transaction fee if I withdraw money. 1 of them, I have to transfer money from loan account to saving account when I want to withdraw money.

My friend told me that the loan spread rate is lower the better. My sister told me that locked in period is shorter the better. My wife has another opinion, she thinks that easier to withdraw money is better. When they were explaining to me, i felt so confusing

. To me very simple, the total rate (base + spread) is lower the better, so that I can pay few monthly installation, but I am not so sure.

Any sifu can guide me how to choose a good loan package?

Dear,

It really depends on your objectives.

1. lowest spread rate will be the given best option, however, it is not a fool proof in this system. Because bank can adjust base rate in the end to increase the effective lending rate. However, choosing the lowest spread rte now could be the best option.

2.

If you have huge cash flow transacting in and out weekly, then full flexi would be a good option for you, because you can credit the amount into full flexi account and withdraw it the next day when you need it. SAVING 1 OR 2 DAYS OF interest in between. If you don't have huge cash flow transacting frequently, then semi flexi is the choice.

However, it really depends on what you want, do read below and choose wisely

Full flexi and semi flexi description will be shown at below:

CODE

Full flexi:

1) current account tied to loan account

2) auto debit from current account at month end and interest is calculated based on outstanding balance minus amount in current account

3) maintenance charge of RM10 per month

4) setup/ processing fee of Rm200 (certain bank)

5)The liquidity comes in the form of an ATM card or a linked CASA account to the housing loan.

Example: You have a shop that is opened Monday to Satuday, rest on Sunday. On Saturday, you deposit all your proceeds of the week into the flexi account, on Sunday, you would save [(your-HL-interest-rate)/365]*AmountDeposited worth of interest. On Monday, you withdraw the money to run your business

6) Withdrawal of money or crediting of money through ATM,CHEQUE,OVER THE COUNTER, or online

Semi Flexi

semi flexi package typically has these features:

1) requires you to phone in to indicate the extra payment as early settlement of advance payments

2) if you fail to indicate, you will be charged 1% (some banks do this afaik)

3) if you indicate advance payment, no additional interest is saved as "advance" payment will only be credited to your loan account when it reaches your cycle date, so it is plain advance payments. and must be in multiple of your monthly payment.

4) For redrawable prepayments, you need to indicate separately and Redraw charge of RM50 is imposed (M*B charge Rm25)

5) Withdrawal of money or crediting of money through Cheque or Over the counter

3. Lock in period.

Lock in period doesn't affect people who stay it in the property forever, if you are a flipper and wants to trade your property in the near short future, then short period lock in period will be beneficial to you.

We never knows what future might holds, so it is wise to choose the shortest lock in period, incase we need to sell or refinance for emergency.

Cheers

Jul 18 2016, 08:18 PM

Jul 18 2016, 08:18 PM

Quote

Quote

0.0249sec

0.0249sec

0.56

0.56

6 queries

6 queries

GZIP Disabled

GZIP Disabled