QUOTE(chewinggum2 @ Mar 4 2022, 06:13 PM)

hi, total newbie here.

how do i know what is my eligibility to get house loan approval?

im a sole proprietor in my 30s looking to purchase a new house/condo.

Generally, everyone should be able to get a loan if he is not blacklisted by a financial institution.

The next question is how much can you allocated you monthly 'salary' for the loan. Then only you will roughly know how much you can borrow and what property price range you can buy.

When you submit your loan application, bank will assess your eligibility based on other outstanding loans ... HP, PTPTN, CC and PL. If none than is straight forward.

In addition, the bank will also consider the market value of the property. If you buy at 500k, and if the bank valuer says is only 460k, then the loan is based on 460k.

For first time loan borrower, he can get max 90% of value or lower if you doesnt qualified for 90%.

So you have to topup the difference with your savings if property value is lower and loan is less than 90%

If you want lower than 90, you pay more downpayment and monthly repayment will be lower.

Monthly repayment amount also depends on age. An older borrower will pay a higher monthly repayment.

Once everything is confirm, the bank will issue an offer letter with the terms. Is non negotiable .... either you accept or reject.

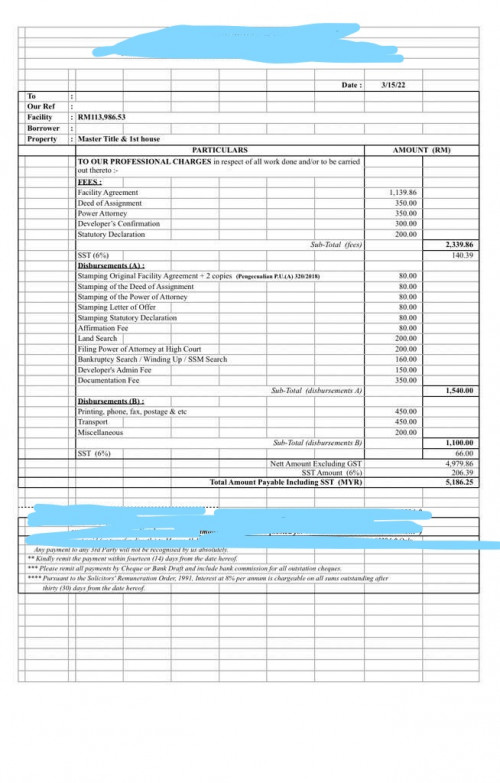

There will be other cost when one purchase a property ..... legal fees, stamp duties, valuation fees (if subsale) and mrta (life insurance for the loan). Remember to allocate some money for that. .... about 5% of purchase price plus the minimum 10% downpayment.

Once you take over the property, you will require some money to reno and furnish the place. There is no limit on how much you want spend. Bear in mind that what you spend doesnt mean you will get back when you sell later.

Since your income is from the sole prop business, make sure all your financial records and tax payment are in order for the bank to review. Having a monthly epf contributions helps....not pay one or two lump sum in one year.

Finally, buy within affordability. The bank can loan you money and they can also auction your property if you dont pay your loan.

Feb 23 2022, 06:11 AM

Feb 23 2022, 06:11 AM

Quote

Quote

0.5658sec

0.5658sec

0.24

0.24

7 queries

7 queries

GZIP Disabled

GZIP Disabled