QUOTE(nujikabane @ Aug 30 2015, 07:13 PM)

Can I get a confirmation that only ILP-linked insurance have the flexibility to add/remove riders ?

Other types of insurance e.g. life insurance, term insurance do not have such flexibility ?

Traditional policy able to add rider as well. However, it do not have the flexibility like investment linked to add/remove after the policy inforce.

QUOTE(nujikabane @ Aug 31 2015, 08:28 PM)

How is Takaful different from other conventional insurance?

e.g.

price

coverage

& does takaful also have investment-linked insurance ?

Yes, Takaful do have investment linked insurance. It's similar to Conventional however, there are a numbers of principle difference between takaful and conventional.

Takaful1)Takaful is based on mutual cooperation.

2)Takaful is free from interest (Riba), gambling, (Maysir), and uncertainty (Gharar).

3)All or part of the contribution paid by the Participant is a donation to the Takaful Fund, which helps other Participants by providing protection against potential risks.

4)Takaful companies are subject to the governing law as well as a Shari’a Supervisory Board.

5)There is a full segregation between the Participants Takaful Fund account and the shareholders' accounts.

6)Any surplus in the Takaful Fund is shared among Participants only, and the investment profits are distributed among Participants and shareholders on the basis of Mudaraba or Wakala models.

7)In case of the deficit of a Participants’ Takaful Fund, the Takaful operator (Wakeel) provides free interest loan (Qard Hasan) to the Participants.

8)The Plan Owners’ and shareholders’ capital is invested in investment funds that are Shari’a compliant.

9)Takaful companies have re-insurance with Re-Takaful companies or with conventional re-insurance companies that adhere to certain conditions of Shari’a.

Conventional1)Conventional insurance is based solely on commercial factors.

2)Conventional insurance includes elements of interest, gambling, and uncertainty.

3)The premium is paid to conventional insurance companies and is owned by them in exchange for bearing all expected risks.

4)Conventional companies are only subject to the governing laws.

5)Premium paid by the Policyholder is considered as income to the company, belonging to the shareholders.

6)All surpluses and profits belong to the shareholders only.

7)In case of deficit, the conventional insurance company covers the risks.

8)The capital of the premium is invested in funds and investment channels that are not necessarily Shari’a compliant.

9)Conventional insurance companies do not necessarily have re-insurance with re-insurance companies that abide by Shari’a principles.

https://www.tazur.com/takaful-vs-conventional.htmlQUOTE(frosteer @ Sep 1 2015, 09:47 PM)

Quick Question =))

Medical card usually cover organ transplant (kidney, lung, liver, heart, pancreas & bone marrow) However, it only covers the surgery cost but does not cover the organ.

Is this correct? Please advise, thanks =)

By the way, is there any AIA agent here can help too?

I heard the latest AIA medical card (sample: R&B200, annual limit 1.375 million, lifetime no limit)

covers both the organ transplant surgery cost and also the cost of the organ. Is this true?

As pointed out by @adele123 , it's not covering the cost of organ. Most of the medical cards are not covering the surgical cost of removing the organ from donor, but some of the premium medical card does. Example: Great Eastern's Smart Premier Health.

QUOTE(polarzbearz @ Sep 1 2015, 10:50 PM)

Hi all, thinking to get my first personal medical insurance as currently I only have the company benefits' one. Anyone have any good recommendation of product or is there any agent here that can PM me?

I'm mostly keen on non ILP-linked medical insurance (traditional type), but I'm open to suggestions. Thanks in advance!

pm-ed you.

QUOTE(kutitata @ Sep 2 2015, 09:55 AM)

Guys,

I am looking to buy medical insurance for my wife and young daughter, I am deciding between AIA and GE...

Both are for Room rate of either 200 or 300 and 1m yearly and no lifetime limit.

However was advised to check the details of GE as they said for GE only the initial amount is paid directly and the balance you have to pay first and claim from GE.

Another concern is that GE has payor benefit for both wife and baby plan but AIA has payor benefit only for baby and not for wife plan.

Can anyone clarify? I need some honest opinion on a good medical plan for my small family.

On the admission to hospital, if Guaranteed Letter is granted by Great Eastern,

full hospitalization bill will be paid instead of paying the initial amount only. This procedure is same across the insurance industry.

As for the payor benefit, it's depends on the attachable rider from the quotation system. AIA are unable to attach payor benefit maybe due to low budget or high insurance chargers from other riders.

QUOTE(polarzbearz @ Sep 2 2015, 10:39 PM)

Interesting, I was offered similar product also from

AIA. Not sure if it's worth to take it up as I currently do not own any personal medical insurance, and are only having company's group medical benefit.

[attachmentid=4873152]

Anyone can comment on this plan?

QUOTE(polarzbearz @ Sep 3 2015, 09:41 AM)

Yup my company group plan is under AIA.

Is it OK compared to, say, the tokio marine you shared earlier? The TM ones looks like similar benefits but cheaper as age grows

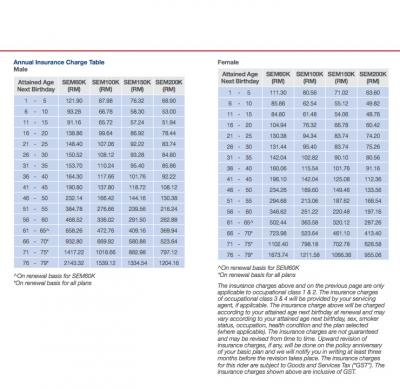

If you are going for deductible plan, why not Smart Extender Max, the price is more affordable, refer to the attachment below.

However I wouldn't advise you to go for deductible plan if you are able to afford at least RM200/month. The reason because

1)The price is not too big different RM100 vs RM200

2)You are taking the deductible risk.

3)Deductible plan might not too suitable for retirement purpose when you are retired without company medical coverage.

4)It's extremely hard for you to get a standard medical card if you are planning to get on your retirement which is age 55.

5)If you are able to get one, high blood pressure/ blood sugar/ cholesterol might made you paying 100% or higher premium rate than normal person. Example: If a healthy age 55 person are paying RM300/month, you might be paying RM600/month due to loading.

Sep 3 2015, 01:21 AM

Sep 3 2015, 01:21 AM

Quote

Quote

0.0367sec

0.0367sec

0.65

0.65

6 queries

6 queries

GZIP Disabled

GZIP Disabled