QUOTE(yklooi @ Nov 4 2013, 12:27 PM)

so, NEVER selects funds solely based on mgmt fees alone.

so is posting of "No matter how many years your time horizon is, any fees or charges on your investment is not good, so go for the lower one" is WRONG to be the sole basis of selections..

Ok ok.. I thought people here are mostly experience investors... It looks like I must word them correctly like a legal document

If not sure kena kau kau.. despite the good intentions and the time spent to justify by being transparent in the calculation...

"

Assuming risk is the same, no matter how many years your time horizon is, any fees or charges on your investment is not good, so go for the lower one"

QUOTE(yklooi @ Nov 4 2013, 12:26 PM)

i believes FSM do have some bonds funds with better (or less) Annual Mgmt fees. than 0.75% (ex AmIncome, KAF, RHB Is inc)

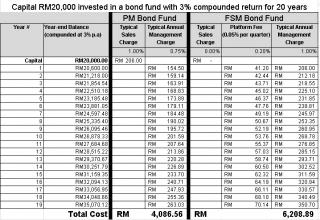

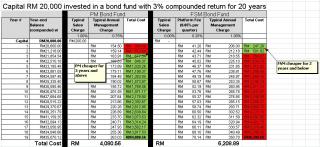

Public Mutual Enchanced bond fund is also 1%?

Also, in my calculation spread sheet, you will see the word "

typical" as in "

typical management fees"

Btw, Public Enhanced Bond fund has equity exposure, I think that's why they are charging higher.

This post has been edited by creativ: Nov 4 2013, 12:46 PM

Oct 31 2013, 10:08 AM

Oct 31 2013, 10:08 AM

Quote

Quote

i am not picking on you. Each is free to express its own...i am just questioning/seek to clarify on the phrases that which i think is misleading/misinterpreted.

i am not picking on you. Each is free to express its own...i am just questioning/seek to clarify on the phrases that which i think is misleading/misinterpreted.

0.0468sec

0.0468sec

0.63

0.63

7 queries

7 queries

GZIP Disabled

GZIP Disabled