Oh, now I know why some people in /kopitiam felt raynmann’s post was sarcastic!

Personal Financial Management V3, It's all about managing your $$$

Personal Financial Management V3, It's all about managing your $$$

|

|

Apr 24 2020, 07:53 PM Apr 24 2020, 07:53 PM

Return to original view | IPv6 | Post

#1

|

Senior Member

7,847 posts Joined: Sep 2019 |

Oh, now I know why some people in /kopitiam felt raynmann’s post was sarcastic!

|

|

|

|

|

|

Apr 25 2020, 10:10 AM

Return to original view | IPv6 | Post

#2

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(farizmalek @ Apr 21 2020, 02:12 PM) » Click to show Spoiler - click again to hide... «  Average monthly Expenses (in times of COVID-19) Cluster Detached Landed Residence monthly maintenance/sinking fund: $1,500/pm Private home lift servicing, pro-rated: $200/pm Utilities (water/electricity/waste disposal): $300/pm Property Tax on primary residence (owner-occupier preferential rate, pro-rated): $400/pm Road Tax: $199/pm x 2 = $398/pm Petrol costs: $250/pm x 2 = Charity donations (combined): $2,000/pm Meals (we hardly - ok, never - cook): Local part-time cleaners: Hobbies/Club membership expenses: Overseas travel (tickets, hotels, food) pro-rated: Discretionary spending: $1,000/pm * ** Without taking our Singapore/Australia tax burdens into consideration, it looks like our outgoing expenses are about This post has been edited by hksgmy: Apr 26 2020, 08:45 AM |

|

|

Apr 25 2020, 09:12 PM

Return to original view | IPv6 | Post

#3

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(farizmalek @ Apr 25 2020, 08:11 PM) Hoep you and your family will be ok during the MCO time. Thank you for the kind thoughts. Yes, my wife and I are OK. Income has dropped about 30% for me (since I’m in private practice and I can’t see my patients from ASEAN since the start of the outbreak), but she’s still drawing her full salary (for now haha). Take care and have a blessed and peaceful Ramadan! |

|

|

May 5 2020, 09:18 AM

Return to original view | IPv6 | Post

#4

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(bagazaru @ May 2 2020, 01:53 AM) Hi all, I was wondering if anyone can help us to further save more and maybe earn more Hello. Both of you are still very young (for reference, I'm a couple of years away from turning the big 50). Most people around your age are able to cope with a little more volatility - I see most of your spare cash is put away at "safe" sources. Safety means a smaller dividend. If you have the appetite for a little bit more risk, the recent market bloodbath might present with a couple of good bargains (banking stocks, for example). Having said that, please do your due diligence - I recently liquidated a couple of HSBC Bonds which were bought close to par/IPO value when the prices went up to 1.08, so I made a little on capital gains, and also reaped the coupons for the few years I held them - this was before the Hin Leong saga erupted and HSBC was caught out to be the biggest lender with over USD600m in exposure. The bond price has come down quite a bit from the 1.08, and while I could have continued to hold on to the bonds until the callback date, I wouldn't have enjoyed the capital gains had I done so. » Click to show Spoiler - click again to hide... « So, due diligence is important - and never buy on a rumour or a whim, or the recommendation of your favourite relative. I buy my bonds through 3 bankers that I've come to trust (as they've aligned their recommendations to my admittedly conservative nature), and I'm glad to say they also keep a keen eye on the bonds' performances and update me accordingly. Please don't get me wrong - I'm not suggesting you pull out of the "safe" assets and plonk everything into riskier ones - but diversification is better tolerated for someone of a younger working age (because you have a longer ability to work & pay off the risk), compared to someone like me. Your ASB funds are definitely worth keeping, as that's paying far higher interest rates than any FD. Good luck! |

|

|

May 5 2020, 09:23 AM

Return to original view | IPv6 | Post

#5

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(honsiong @ May 2 2020, 04:54 PM) Going through this thread, I can't help but feel there are so many ppl humblebragging here. Those earning >10k have no business sharing or pretend to ask for advice here, you are only bragging and trolling trying to make ppl here feel bad. Erm... respectfully, I beg to differ. I would imagine, those earning more than a certain amount (I wouldn't arbitrarily peg it to a fixed figure) should share their insights or opinions so others can pick and choose what works for them. Earning > 10k, you are totally not in a pinch needing help managing money, you only need to not fuck up your business and income source, and don't waste money on lambo or mont kiara condo. When facts are stated well, factually, then that's not a boast - and I can't make you feel bad if you're not the one feeling the hurt. Then again, the above is just my humble opinion - feel free to disagree. That's what a forum like this one is for. |

|

|

May 7 2020, 06:10 PM

Return to original view | Post

#6

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

I’m not the best person to offer specific advise because of the positively lopsided remuneration I enjoy - as someone on this section has mentioned, I could effectively opt for safer, lower yield asset classes because I could “bulldoze” my way though the sheer size of my savings pot. However, that aside, I believe in a few general rule of thumbs to live by: 1. Never be afraid of hard work: when I was a junior medical officer, while studying for my specialty exams, I did locum work at various hospitals and clinics. I was much younger and physically stronger - the night shifts were perfect because I could study while waiting for patients to come in - essentially I was getting paid to study. If you feel up to it, do free-lance or part time work. You’ll never know what the networking or connections can become useful in the future. 2. Always live below your means - make it a point to delay your gratification. I bought my first car in Singapore and drove the wheels off it. We continued to live in our HDB until our previous neighbours moved out and the new ones that moved in got into trouble with the loan sharks. Otherwise, I would never have moved into private housing. 3. Never ever spend money you don’t have on things you don’t need to impress people you don’t know. And those you know shouldn’t need you to put up a false front to impress them. 4. Have a realistic and honest analysis of what your risk level is and don’t try to overachieve your targets - meaning to say, if you really don’t have the appetite to punt on stocks because you’re afraid of losing your capital, then don’t. I only ever buy IG rated senior subordinated bonds - the yields are relatively modest but even in the midst of this COVID19 turmoil, I’m sleeping really well at night. I do have a smaller portfolio of blue chip stocks that I’m holding for their dividends, but that’s the limit of what I’m comfortable buying. 5. People always talk about leverage and I know there are 2 schools of thoughts on this, but I don’t subscribe to that particular philosophy. All my properties, bonds and stocks have been fully accounted for - no outstanding loans, no mortgages, no risk of margin calls. Granted, if my wife and I had utilised leveraging as a means for wealth generation years ago, we could have doubled our wealth or doubled the properties we presently owned - but then, we might still be in debt. There’s no one single size that will fit everyone - I’m just offering my perspective for discussion. Good luck! MedElite23 liked this post

|

|

|

|

|

|

May 9 2020, 10:12 PM

Return to original view | IPv6 | Post

#7

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(MalaysianFire @ May 9 2020, 06:26 PM) The 21k I listed that of my cash on hand is listed there, the 6 months emergency cash is already part of it and it's easily accessible when I need it. The high yield savings account is paying decent, a bit higher than FD. Well done on your plans!Hahaha, OPR just cut. The FD rate now is so low. Ready to take on some risk to see some growth, guess now is a good time since younger can tolerate more risk .. |

|

|

May 10 2020, 10:24 AM

Return to original view | IPv6 | Post

#8

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

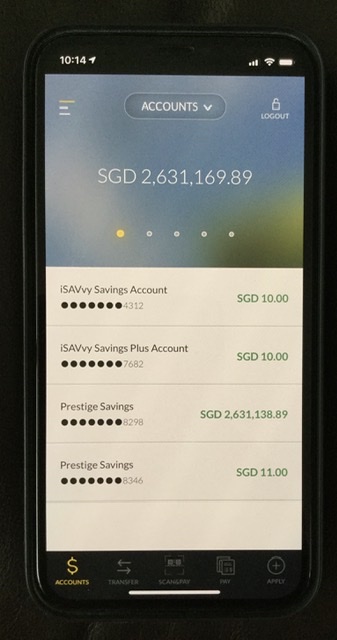

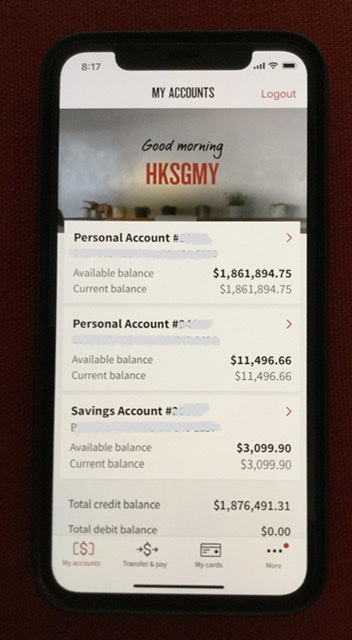

QUOTE(brokenbomb @ May 9 2020, 10:21 PM) I know I memang kena flame for this but ya, my emergency cash are almost 90% in unit trust. I’m a self avowed ultra-conservative investor. When I say emergency funds, I mean the most liquid of all liquid assets - short of stashing physical notes like Najib in his house - I have them in high yield accounts that I ping-pong every 2 to 3 months to take advantage of the promotion rates. Yes drawdowns due occur but I just have to ride this through until next year. But selagi still ok, continue doing RSP ja Not even in FD (which I do have money locked up as well). Here are 2 examples - one is with Maybank Singapore, the other is with NAB: » Click to show Spoiler - click again to hide... « And yes, my NAB account bears my lowyat forum nickname. I thought it to be a nice touch. My UOB accounts have also been renamed to my lowyat nickname too haha. This post has been edited by hksgmy: May 10 2020, 10:32 AM |

|

|

May 10 2020, 10:38 AM

Return to original view | IPv6 | Post

#9

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(brokenbomb @ May 10 2020, 10:34 AM) 3% of a million is already 30k. Haha. SGD deposit rates are way lower. I’m getting less than 2% on my SGD savings - but it’s a trade off for being highly liquid. I’ve already drawn down quite a bit during the recent stock market turmoil due to COVID 19, and picked up a few good IG bonds below IPO price as well as a few banking stocks that I’ve been eyeing.But mine is only in the 4 figures, So maybe my risk profile is different 😅 But then again after i reach that 1 million mark, I might be looking at FD or filling up my asb 1 and 2. |

|

|

May 10 2020, 01:27 PM

Return to original view | Post

#10

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(MalaysianFire @ May 10 2020, 01:01 PM) wow. nice. even dividens alone from the savings accounts can keep you going in terms of expenses. If you don't mind, may I know how long you have been investing already ? Yes, my wife and I’ve been lucky to both share decent salaries coupled with frugal habits. And we have also been lucky with some of our property purchases, before all these additional stamp buyers duties and taxes came into force. Overall, we’ve started investing in IG bonds and blue chip stocks for the past decade or so, after we paid off all our property purchases in Singapore and Australia. All our properties are mortgage-free and are tenanted, which also makes for a good passive income stream. Both my wife and I are a couple of years away from turning 50, so I believe we are much older than most of you here. Good luck! |

|

|

May 10 2020, 02:19 PM

Return to original view | Post

#11

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(HumbleBF @ May 10 2020, 01:48 PM) May i know at what age have you started working in the workforce? and what age did you start investing in properties? I started working at 25, after I’d completed my medical degree. I am now a consultant medical specialist in private practice. My wife is a chartered accountant. We bought our first investment property nearly 17 years ago. I was able to pay the instalments from my locum income. My wife and I both work in Singapore, so admittedly, the remuneration packages were considerably more generous. |

|

|

May 10 2020, 03:40 PM

Return to original view | IPv6 | Post

#12

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(jasontoh @ May 10 2020, 02:23 PM) Able to have such networth working class also consider a big achievement. I'm not sure how many of us here would be able to save that much (at least in savings account) Indeed, my wife and I consider ourselves very fortunate. A rule of thumb for us is that we keep at least 10% of our net worth in a highly liquid environment (not even FDs) - and that means either as cash or in a high yield/savings account. You’ll never know when you need to use money urgently, or if a good bargain emerges in the market. During the recent COVID19 induced market upheaval, we bought more than $1,000,000 worth of good quality Singapore bank bonds (DBS, OCBC and UOB) at between 98 to 99¢ - which was even lower than their IPO prices! I already have bonds of these banks bought years ago, and I’ve had to pay way more than 98¢ for them, that’s for sure!And that is the primary reason why we steadfastly follow a conservative bias when it comes to investing - because every cent is hard earned money, from much blood, sweat and tears. Moreover, we are not young anymore and correspondingly, our risk appetites are also lower, given the difficulty of recouping losses from risky stocks or margin calls gone bad. Hence, we don’t leverage and we don’t believe in risky assets. This post has been edited by hksgmy: May 10 2020, 03:47 PM |

|

|

May 19 2020, 07:05 AM

Return to original view | IPv6 | Post

#13

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(leo_kiatez @ May 18 2020, 06:29 PM) Well and far-sighted!! Do u still live in Malaysia? No we don’t, we’ve been based in Singapore for nearly 30 years. I’m still Malaysian though, She’s taken up Singapore citizenship. |

|

|

|

|

|

May 19 2020, 09:20 AM

Return to original view | Post

#14

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(woonsc @ May 19 2020, 07:54 AM) Do you pick individual bursa stocks? No we don't ... to be honest, I've been away too long to know the "feel", as such, it's not worth taking a punt. |

|

|

Jun 5 2020, 10:53 PM

Return to original view | IPv6 | Post

#15

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(cloudstrife07 @ May 28 2020, 03:53 PM) Hey guys, Just to update and share that when there's a will, there's a way! Syabas and Selamat Hari Raya!I'm happy to report that I've managed to settle one card already based on my above enquiry. Next month will start paying the second card. I even almost didn't celebrate Hari Raya  Was deciding either to finish paying next month and enjoy raya or pay everything this month for that card and have a simple raya with family (I mean really simple, just cook some rendang, photoshoot and that's it. No visiting relatives and new baju raya etc.). End of the day I chose the latter and and after a week, I felt it's the better choice! Was deciding either to finish paying next month and enjoy raya or pay everything this month for that card and have a simple raya with family (I mean really simple, just cook some rendang, photoshoot and that's it. No visiting relatives and new baju raya etc.). End of the day I chose the latter and and after a week, I felt it's the better choice! |

|

|

Jun 5 2020, 10:55 PM

Return to original view | IPv6 | Post

#16

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(coolguy99 @ May 19 2020, 10:29 AM) Very nice to be able to retire in Singapore comfortably. Perhaps, but we will be migrating over to Sydney soon, to enjoy our (semi) retirement. I am envious. I am envious. |

|

|

Jun 6 2020, 10:40 PM

Return to original view | IPv6 | Post

#17

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(daidragon12 @ Jun 6 2020, 10:36 PM) Which part of Sydney? I was there 2010-2015. Stayed around maroubra/eastgardens. Very nice place - quiet, close to beach, nice people. Sorry for being off-topic. We have a couple of properties there - one at the Lower North Shore, another at Double Bay and the third in the Inner West suburbs, over looking Rozelle Bay. As it stands, I’m leaning quite heavily towards our house in the Inner West, but my wife is keen to renovate the house at Double Bay. We still have a couple of years to sort out the final decision, besides, all the properties are currently tenanted.This post has been edited by hksgmy: Jun 6 2020, 10:41 PM |

|

|

Jun 16 2020, 11:41 AM

Return to original view | IPv6 | Post

#18

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(tripleA+ @ Jun 16 2020, 11:39 AM) High five!! You have made it in your life .. At my age (nearly 50), I would like to think that I've worked hard all my life to get here. There's still a lot of insecurity - I guess it's just my nature - what with impending (semi) retirement, and what if we fall ill (outside of whatever the insurance can cover) etc, but I'm naturally a worrier anyway. Just need to learn how to worry less. |

|

|

Jun 17 2020, 10:08 AM

Return to original view | IPv6 | Post

#19

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(tripleA+ @ Jun 16 2020, 02:33 PM) I assume everything else all cleared eg children grown up independent/adequate coverage of properties which you mentioned fully paid off and avoid major scammer which will ruin you financially/emotionally..you are in great shape Yes, we have no outstanding loans or mortgages on any of our properties, and we have no kids (DINKs) - so, in that sense, no worries about education costs etc. Since we became debt free about 10 years ago (at 40 years of age), there's a kind of satisfaction to be able to count every day as a profitable day - whenever a bond coupon is paid, that's profit. Whenever a FD interest payment is due, that's profit. Whenever a tenant pays his rental, that's profit. Interestingly, that's also when we stopped purchasing residential properties for investment purposes - partly also because of the realization that properties come with quite a lot of additional costs (stamp duty, seller duty, additional stamp duty, property tax, maintenance fees, land taxes - not to mention that the income is taxable in both Australia and Singapore), but also because we discovered that IG bonds (senior subordinated, good quality, rated bonds) pay an equivalent amount in %, as are tax-exempt (in Singapore). Since then, our property portfolio has remained more or less stagnant - apart from one house purchase in Sydney for our personal use, and a couple of commercial investments in Sydney as part of our company there - whilst our bonds portfolio has grown exponentially. When we move over to Sydney in a couple of years' time (provided the plans remain the same), we will begin to draw down on the interests/coupons/dividends/rental returns - the capital is expected to remain constant, and God willing, should outlast our lifetimes. |

|

|

Jun 17 2020, 10:35 AM

Return to original view | IPv6 | Post

#20

|

|

Senior Member

7,847 posts Joined: Sep 2019 |

QUOTE(leo_kiatez @ Jun 17 2020, 10:32 AM) Won't the SG bonds turn sour over the years or during tough times? Possibly, but that's a risk with any investment - properties or otherwise.Most of the bonds are with the "big" institutions - UOB, DBS, OCBC for example. I'm not an imaginative man. I stick with what I can understand. And, I understand if DBS, UOB or OCBC go under, then, all the SGD I have under my pillow is probably going to be good enough to be used as toilet paper - and the country will go belly up. The other thing is, as long as these companies don't collapse, and I buy my bonds to hold till old (as I always say), I will always get back the initial $250,000 investment per bond. This post has been edited by hksgmy: Jun 17 2020, 10:36 AM |

| Change to: |  0.0242sec 0.0242sec

0.47 0.47

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 3rd December 2025 - 10:10 AM |

Quote

Quote )

)