[quote=emperor_o4118,Oct 20 2016, 10:01 PM]

Hi all, i recently book house at Sr Sendayan Seremban.

House price - Rm538888

net income me and wife - Around RM4500 joint applicatiom

Finance - 90%

Commitment - car Rm550

credit card - monthly rm175

i have calculated roughly my dsr around 70%, my question how are my chances for my application to be approve? I apply with CIMB, RHB, Maybank n Ambank.

What are other factors that bank consider to approvr my application?Is DSR calculated bank will be higher compare to standard DSR calculation?

[/quote]

Dear

emperor_o41181. HLBB, CIMB, RHB has highest chances

2. DSR is based on the profile you just shown

Bank will also look at your ccris arrears, any CTOS problems, any restructured debts, how many debt facilities you have, your company, your jobs nature of business.. etc. all myriad of factors will be calculated into the credit scoring

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

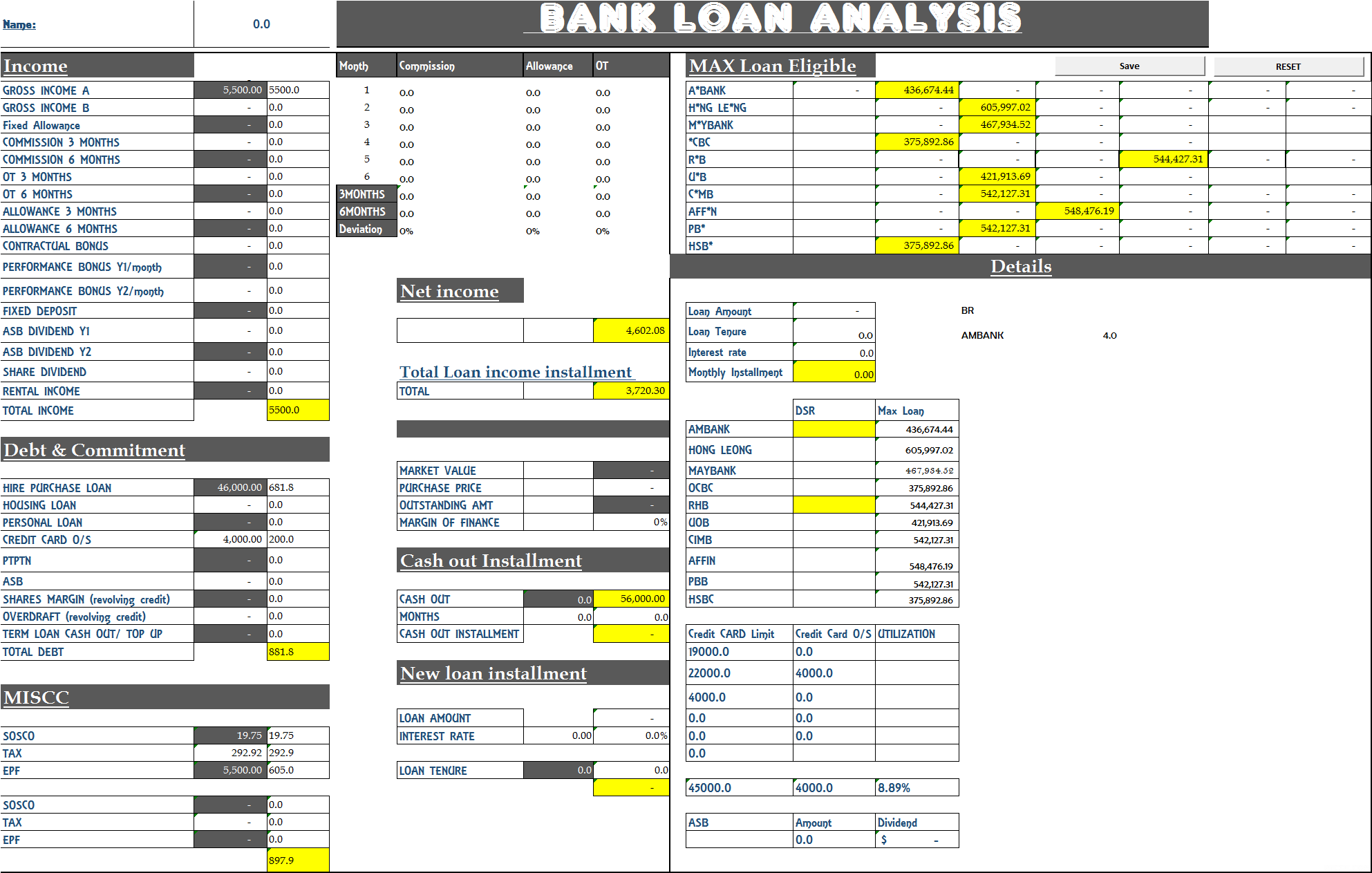

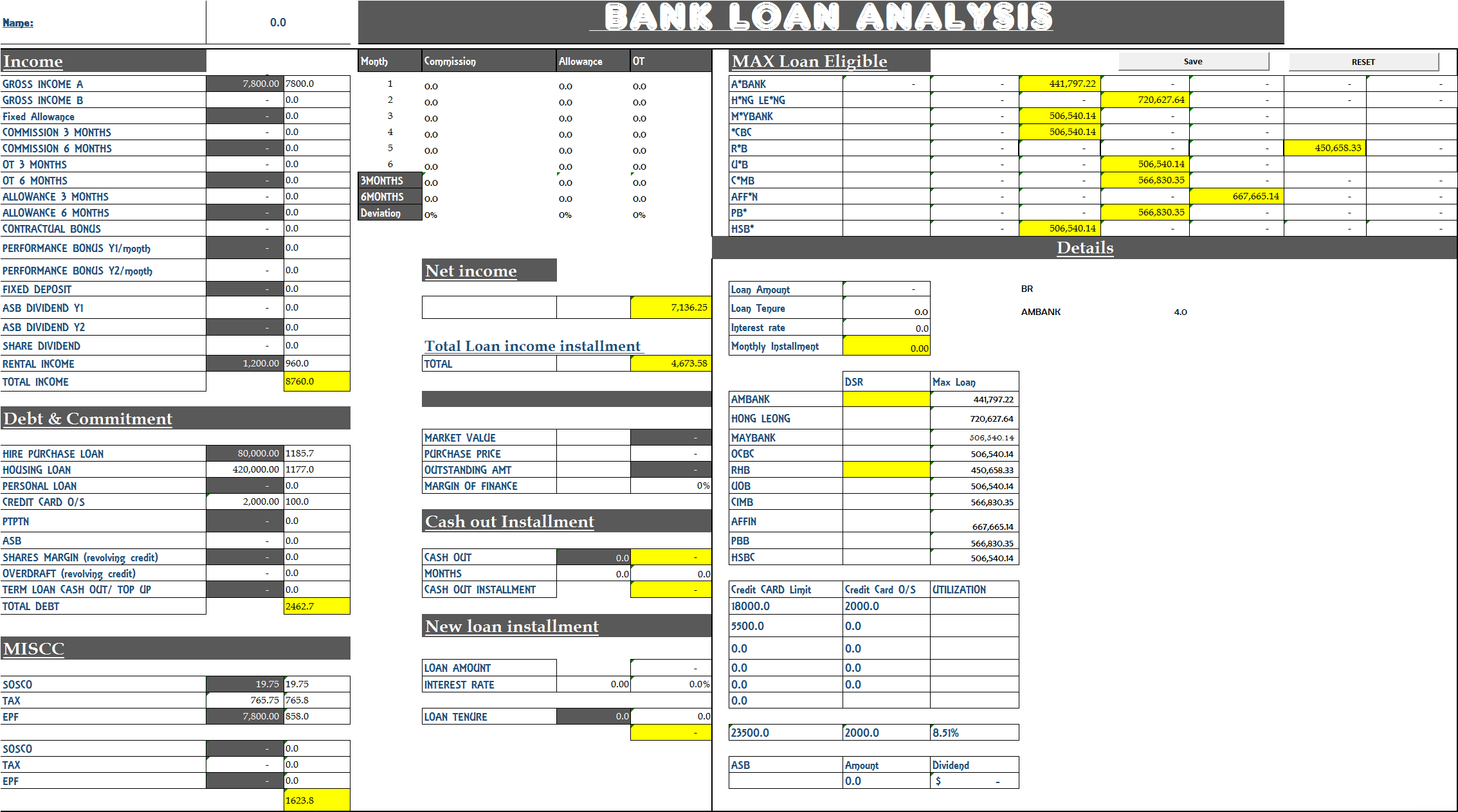

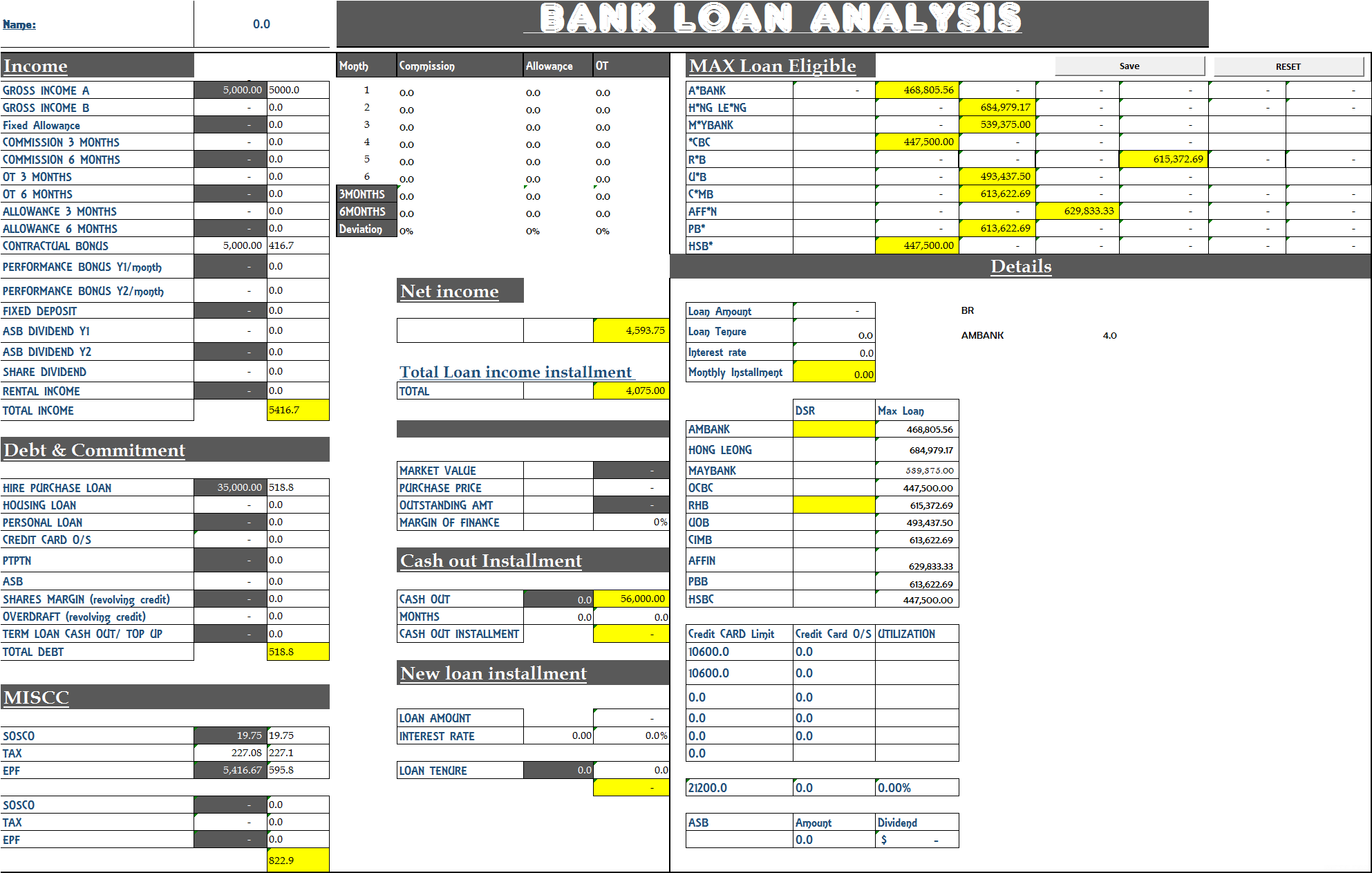

1. Based on the details given by you, Your max loan eligibility for each bank is as follow:

Rm

A*BANK 436,674.44

H*NG LE*NG 605,997.02

M*YBANK 467,934.52

*CBC 375,892.86

R*B 544,427.31

U*B 421,913.69

C*MB 542,127.31

AFF*N 548,476.19

2. The best bank to get the highest loan would be HLBB. However, each bank has it's own ball game

Different bank will calculate your income and debt accordingly based on each bank's different policy. Hence,

I would need to do a due diligence on your profile before suggesting the best bank to proceed with."

3. I would need to check you CCRIS, CTOS and income documentation before giving you any assurance.

If everything goes fine, 90% shouldn't be a problem for you."

4. If you need my help, do feel free to contact me. I will be all ears in guiding you towards this rough path.

5. I have wrote some articles that help guide first time home buyer to get housing loan, feel free to read it at below link:

5 Tips for employee to prepare for loan application Few easy tweaks for self employed and freelancer to ensure loan approved

Cheers

[quote=Nymphetamine666,Oct 21 2016, 01:20 AM]

Dear

Nymphetamine666,

1. it's consider good, but hear me out.

CODE

Dear

Base rate + spread rate = Effective lending rate

Base rate will alter according to banks need from time to time, hence it will affect your EFL

Spread rate will be fixed throughout the loan tenure.

Hence, banker like to say lower spread rate will be better:

Example:

A) 4% + 0.5% = 4.5% effective lending rate

B) 4.1% + 0.4%=4.5% effective lending rate

Both ELR is the same, but the spread rate is different.

Hence in common perspective sense, people will chose the lower spread rate as it is fixed throughout loan tenure. Thus will say B is better.

But actual sense, there's no best solutions or answer for this. Because, lower spread rate doesn't secure the bank from increasing the base rate in the future and ELR is higher than A in the future.

It's very subjective,

For me, if the ELR is the same, spread rate different isn't differ by alot, I will chose according to few criteria as below:

A. Banks that are easily accessible to your vicinity, why take loan offer form bank when you need them, you need to drive 20-40km.

B. Customer services, go with bank that offer tremendous value added service, try calling their hotline whether easily reached and are they responsive and helpful. In long term, this will lessen any unwanted hassle.

C. Semi or Full flexi that suits your criteria. SOmetimes, different banks semi and full flexi mechanism is different

D. Does the loan package has the right features that you need? Finance legal fees, semi/full/fixed/islamic loan ? lock in period or without? defaultment period ? loan account is it link to saving or current account?

E. Does the consultant serves you well?

etc all this that must put into consideration into long term perspectives instead of just interest rate. Effective interest rate right now is quite short term view.

2. It's the same with MRTA... same thing different package but with syariah compliances.

3.

CODE

Full flexi:

1) current account tied to loan account

2) auto debit from current account at month end and interest is calculated based on outstanding balance minus amount in current account

3) maintenance charge of RM10 per month

4) setup/ processing fee of Rm200 (certain bank)

5)The liquidity comes in the form of an ATM card or a linked CASA account to the housing loan.

Example: You have a shop that is opened Monday to Satuday, rest on Sunday. On Saturday, you deposit all your proceeds of the week into the flexi account, on Sunday, you would save [(your-HL-interest-rate)/365]*AmountDeposited worth of interest. On Monday, you withdraw the money to run your business

6) Withdrawal of money or crediting of money through ATM,CHEQUE,OVER THE COUNTER, or online

Semi Flexi

semi flexi package typically has these features:

1) requires you to phone in to indicate the extra payment as early settlement of advance payments

2) if you fail to indicate, you will be charged 1% (some banks do this afaik)

3) if you indicate advance payment, no additional interest is saved as "advance" payment will only be credited to your loan account when it reaches your cycle date, so it is plain advance payments. and must be in multiple of your monthly payment.

4) For redrawable prepayments, you need to indicate separately and Redraw charge of RM50 is imposed (M*B charge Rm25)

5) Withdrawal of money or crediting of money through Cheque or Over the counter

4. If it's over 3 years... yes.

5.

Well they can structure the deal anyway the bank wants, they are doing it monthly payment, payment scheme structured differently.

Dear

1. it's no and it's yes

It depends on if you feel that protection is important to you and your family in the future..

2. For your question, certain bank or branches will required a compulsory must take MRTA if you want to sign the letter offer... coercive...

However, in actual, it's non mandatory...

Cheers

Dear

Not compulsory!

BUying own will do the work.. or just leave that part blank..

Why are you filling the form? thought agent doing that for you! haha

CHeers

[/quote]

Thank you sir.

[/quote]

Dear

Nymphetamine666,

No problem! Hope it helps!

[quote=cwtien,Oct 21 2016, 10:34 AM]

Hi,

I currently have a semi-flexi loan with RHB Bank. I'm looking to convert this loan to a full-flexi loan (RM 1mil over 20 years). I have asked RHB Bank to give me a quote, but they don't seem that interested (maybe because they get to earn less

).

I'm asking regarding:

1) Fees for moving loans across banks.

2) Estimated monthly amount I have to pay.

3) Any other fees.

I can give more details via PM. I don't want to provide full details in an open forum. Basically, I'm asking agents from other banks to contact me with offers if they're interested

[/quote]

Dear

1) Refinance

Legal loan fees RM16245

CODE

Loan amount: 1000000 Sub Total

Professional Charges

Facilities Agreement 7,450.00

Charge Annexure 900

Discharge of charge

Entry and Withdrawal of Private Caveat 350

Statutory Declaration 100

Professional Charge 8800

Disbursement

Stamp duty on the Facility Agreement (Original) 5000

Stamp duty on the Facility Agreement (Copies) 20

Stamp duty on the Charge Annexure 40

Stamp duty on the Discharge of charge

Stamp duty on Letter of Offer 20

Registration Fee on Charge 120

Registration Fee on Entry and Withdrawal of Private Caveat 450

Registration fees on Discharge of charge

Affirming Fee/Bankruptcy Search 100

Stamping on Statutory Declaration (Owner Occupation/not a bankrupt) 40

Land Search 120

Documentation Fee 318

Transportation 300

Telephone Calls, Facsmile, Printing charges and couriers and etc 300

Miscellaneous 50

GST 6% 567

16245

Valuatioan fees around RM2K

16245 + rm2000 = RM18245

2. RM5000

3. as stated at NO.1

Cheers

[quote=Skylinestar,Oct 21 2016, 02:32 PM]

I'm sure CIMB will approve easily

(based on my experience)

[/quote]

oh wow.. confidence.

[quote=snowswc,Oct 22 2016, 01:54 AM]

Hi sifu..

need your advice. i plan to buy a second house located at Damansara Utama. the price is about RM 1m.

My current details are as follow, please guide me on the max. loan amount I will be able to undertake:

Age : 29

Job :Finance Manager

Gross pay : RM 13500

Nett pay : RM10,500

Bonus : estimate 3 months a year

Commitment : Insurance : RM300

House : total RM 2100 (joint loan - remaining 450 months *40 years loan*)

Car : RM 1,500 (remaining 26 months)

Existing Mortgage Loan (JB property)

Loan outstanding : RM 480k

current account (flexi loan) : RM300k cash

monthly payment : mentioned above RM 2100.

Rental income : 1,600

Thank you!!

[quote=snowswc,Oct 22 2016, 02:03 AM]

thanks. may i know what is the best rate currently exist in the market? my existing loan with Alliance, i get 4.27%. would it be good to continue with Alliance combine to get better rate or it makes no difference if i go for another bank?

[/quote]

[quote=snowswc,Oct 22 2016, 02:08 AM]

thanks. i heard some of the banks require the borrower to buy the what MRTA or MLTA insurance, is that truth? because i insist not to purchase any insurance for my JB property and Alliance still approved my loan.

[/quote]

[/quote]

Dear

snowswc1. If GIVEN YOUR ccris has no prolem, 1million loan should be fine and great

2. Do provide me the property market value, so taht i can check whetehr the property value can match the selling price

-Property full address

-square feet

landsize

built up

-Property type

-aNY RENOVATION

3. For your loan amount, best rate can go towards 4.3%, last month 1million loan client of mine receive best rate 4.3%

Unfortunately, alliance.. rate nowadays are bad.. not that competitive as usual anymore..

4. Well, There's no such thing as compulsory! It's optionable for the borrower!

Nothing is compulsory in this world.

--------------------------------------------------------------------------------------------------------------------------------------------------------------

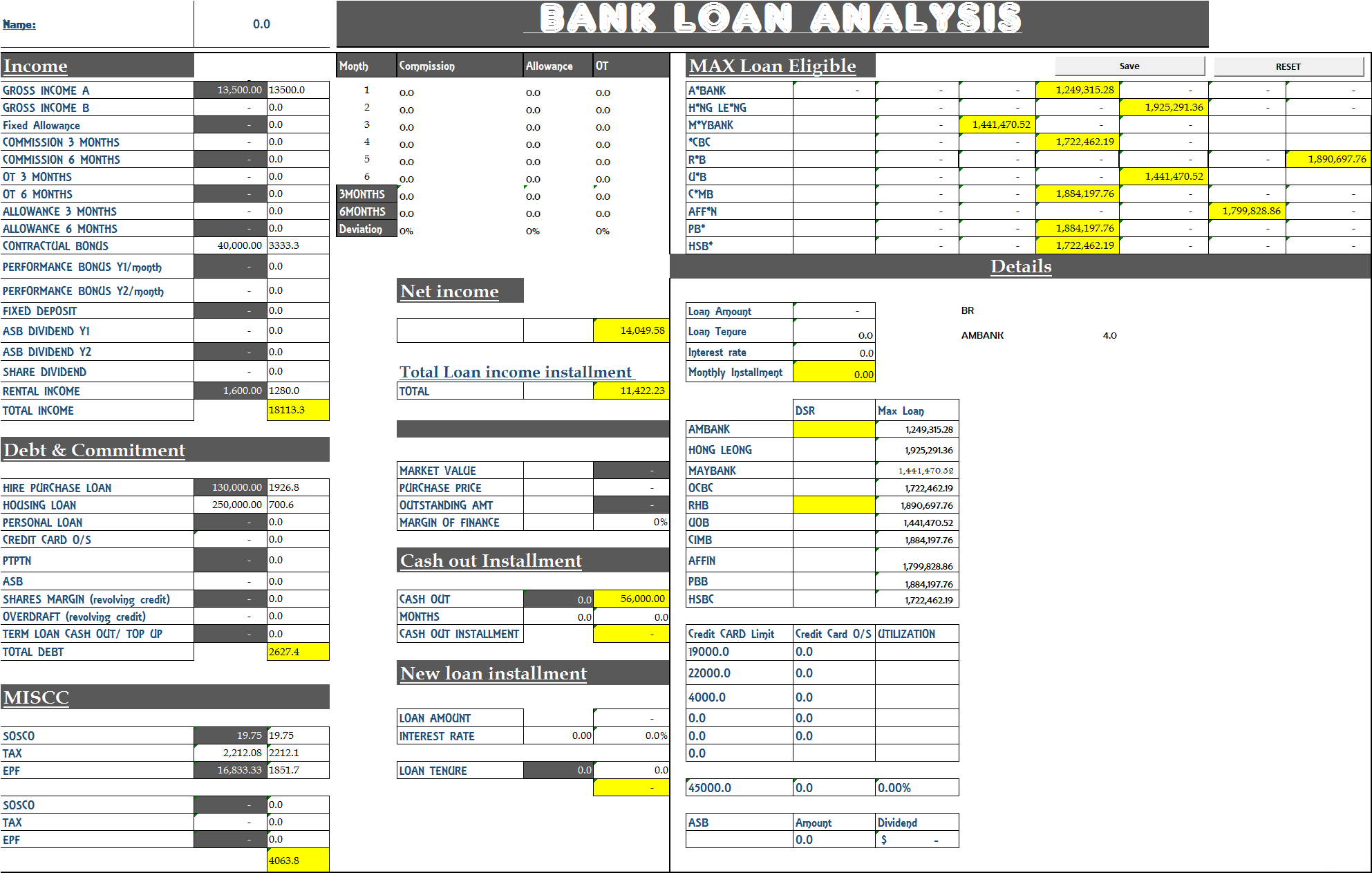

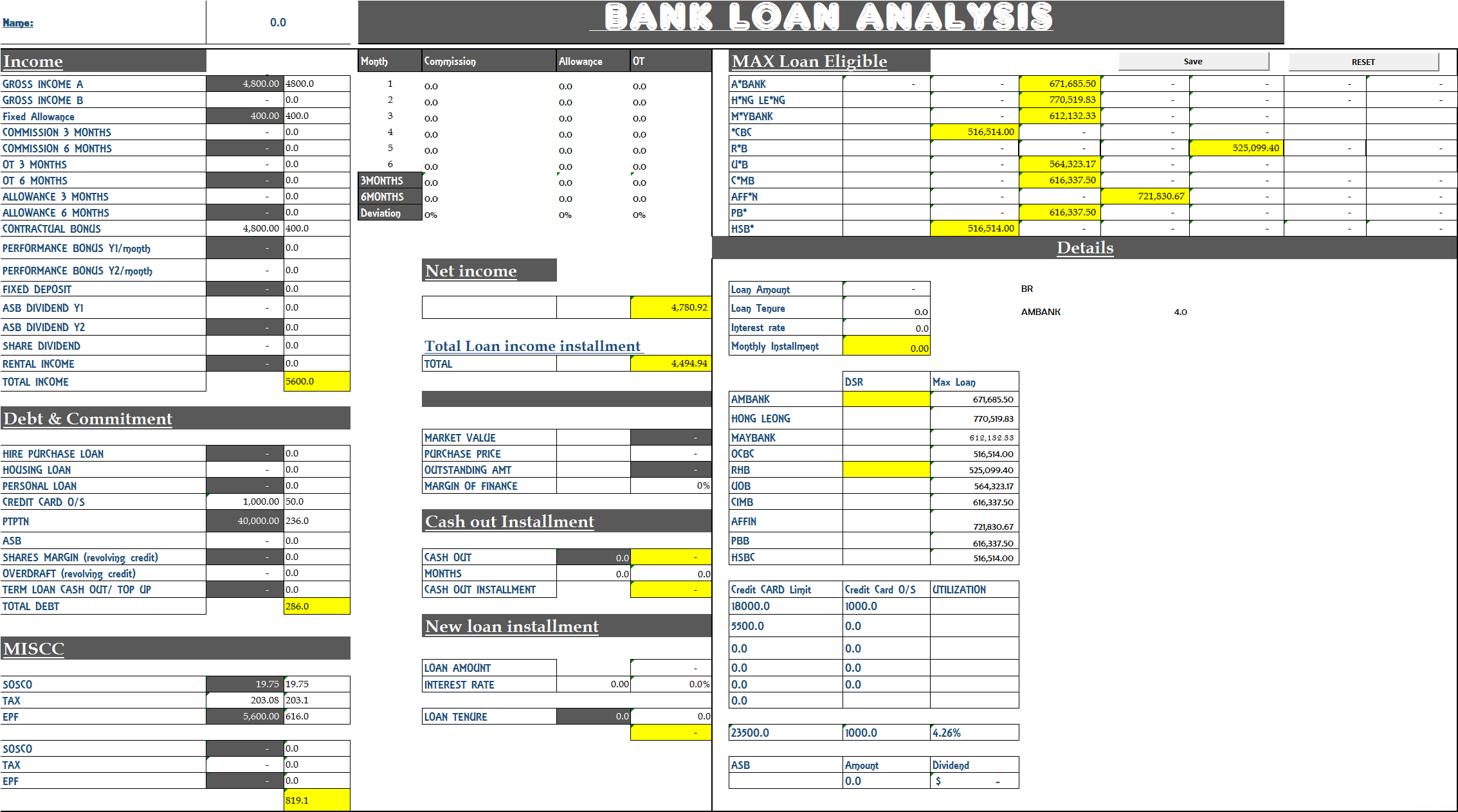

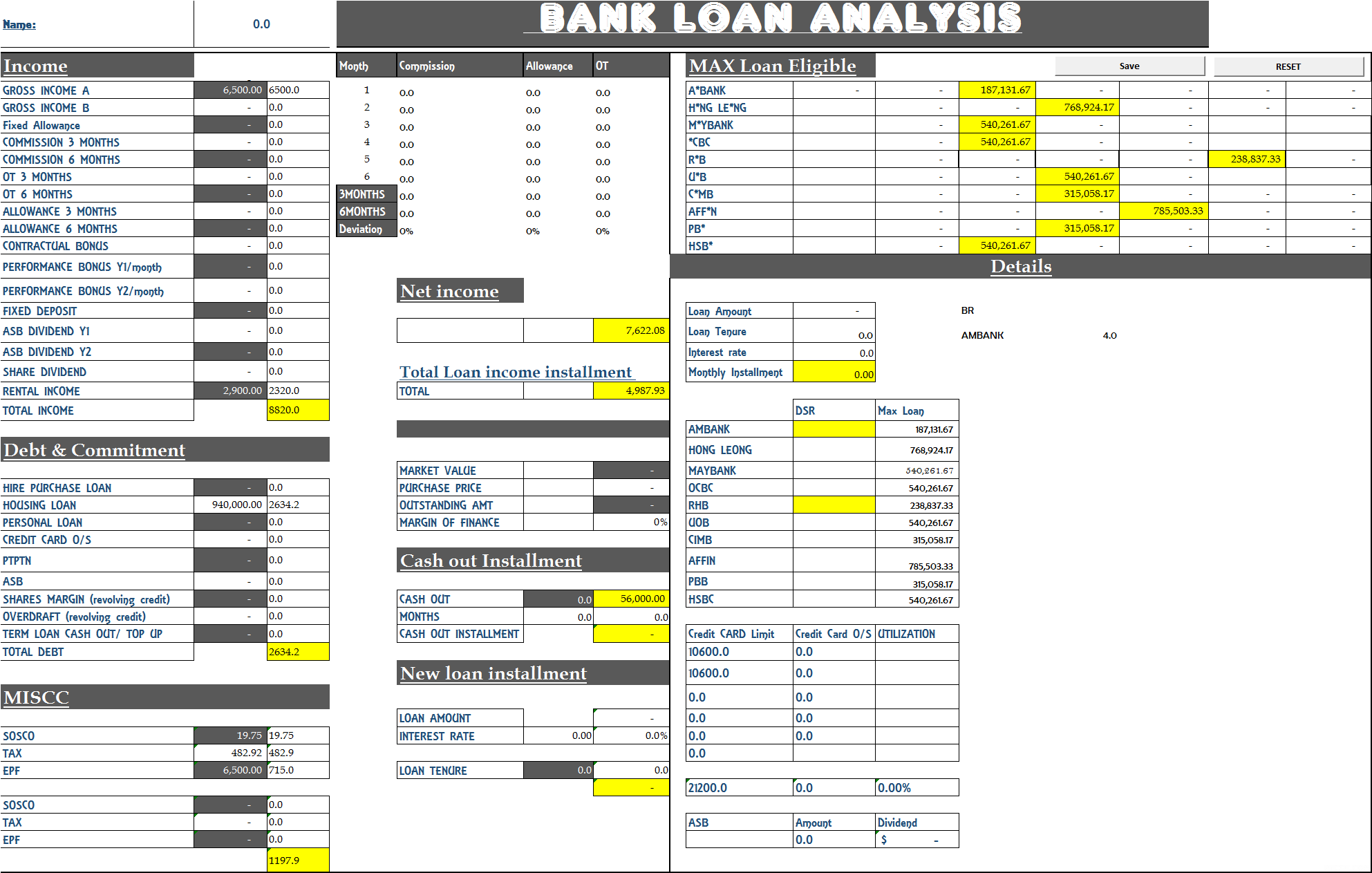

1. Based on the details given by you, Your max loan eligibility for each bank is as follow:

Rm

A*BANK 1,249,315.28

H*NG LE*NG 1,925,291.36

M*YBANK 1,441,470.52

*CBC 1,722,462.19

R*B 1,890,697.76

U*B 1,441,470.52

C*MB 1,884,197.76

AFF*N 1,799,828.86

"2. The best bank to get the highest loan would be HLBB . However, each bank has it's own ball game

Different bank will calculate your income and debt accordingly based on each bank's different policy. Hence,

I would need to do a due diligence on your profile before suggesting the best bank to proceed with."

"3. I would need to check you CCRIS, CTOS and income documentation before giving you any assurance.

If everything goes fine, 90% shouldn't be a problem for you."

4. If you need my help, do feel free to contact me. I will be all ears in guiding you towards this rough path.

5. I have wrote some articles that help guide first time home buyer to get housing loan, feel free to read it at below link:

5 Tips for employee to prepare for loan application Few easy tweaks for self employed and freelancer to ensure loan approved

Cheers

This post has been edited by Madgeniusfigo: Oct 24 2016, 07:09 AM

Sep 19 2016, 03:42 PM

Sep 19 2016, 03:42 PM

Quote

Quote

0.1370sec

0.1370sec

0.44

0.44

7 queries

7 queries

GZIP Disabled

GZIP Disabled