Vote for stagnant 1st half year because most people waiting for election and 2nd half will slightly increase because people back to BBB mode after election.

V10 - Property Prices (Up, Down or .....), and the debate goes on and on and on ...

V10 - Property Prices (Up, Down or .....), and the debate goes on and on and on ...

|

|

Mar 24 2013, 06:54 PM Mar 24 2013, 06:54 PM

|

Junior Member

365 posts Joined: Mar 2010 |

Vote for stagnant 1st half year because most people waiting for election and 2nd half will slightly increase because people back to BBB mode after election.

|

|

|

|

|

|

Mar 24 2013, 07:08 PM

|

|

Senior Member

1,801 posts Joined: Aug 2012 |

QUOTE(lqcevox @ Mar 24 2013, 06:54 PM) Vote for stagnant 1st half year because most people waiting for election and 2nd half will slightly increase because people back to BBB mode after election. I was neutral all the while.... However this weekend I think I'm leaning towards upside already.... LYF famous lawyer super confident correction or crash coming anytime, also jus plunge in to buy a prop at 664psf last week.... Who cares GE coming or not.... Or who says ppl waiting for GE over?.....   This post has been edited by AppreciativeMan: Mar 24 2013, 07:10 PM |

|

|

Mar 24 2013, 07:33 PM

|

|

Junior Member

365 posts Joined: Mar 2010 |

QUOTE(AppreciativeMan @ Mar 24 2013, 07:08 PM) I was neutral all the while.... However this weekend I think I'm leaning towards upside already.... LYF famous lawyer super confident correction or crash coming anytime, also jus plunge in to buy a prop at 664psf last week.... Who cares GE coming or not.... Or who says ppl waiting for GE over?..... Just some of my friends gonna grab a unit of property after election . Most of them listened to these people said properties will DDD mode in 2009/2010 until now they really beh tahan so gonna grab it after election so I assume alot people also like that wait until after election.  Just my own opinion, don't shoot me too hard.  |

|

|

Mar 24 2013, 08:35 PM

|

|

Senior Member

551 posts Joined: Feb 2012 |

BBB mode still in the ACTIVATED mode. One of the project just soft launched for 2 days and 80-90 units or more being booked. Lol. Landed properties with gng concept at rawang. Lol. My vote still simple. UP. Haha

|

|

|

Mar 25 2013, 01:00 PM

|

|

Senior Member

1,780 posts Joined: Nov 2010 |

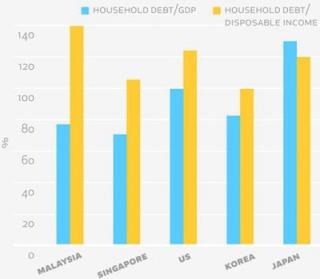

Nice work, we are at the top now. Congratulations.

Attached thumbnail(s)

|

|

|

Mar 25 2013, 01:27 PM

|

All Stars

10,314 posts Joined: Dec 2009 From: Malaysia |

so, shall we buy more singapore and korea's props?

|

|

|

|

|

|

Mar 25 2013, 01:32 PM

|

|

Senior Member

551 posts Joined: Feb 2012 |

household debt is it included car loan/personal loan/study loan?

|

|

|

Mar 25 2013, 02:01 PM

|

Senior Member

2,294 posts Joined: Sep 2011 |

flippers are bbb to sustain their debts mah...

|

|

|

Mar 25 2013, 02:46 PM

|

Senior Member

4,440 posts Joined: Jan 2010 From: Kuala Lumpur |

QUOTE(lqcevox @ Mar 24 2013, 07:33 PM) Just some of my friends gonna grab a unit of property after election Those who said property will slump in 2010 are not the same ppl today. U must learn to differentiate between the doomsday ppl and the real investors. Doomsday ppl will always speak negative bout the property any time and they are usually those who cannot afford high end properties themselves. While the real investors are those who know when and what properties to buy into anytime. . Most of them listened to these people said properties will DDD mode in 2009/2010 until now they really beh tahan so gonna grab it after election so I assume alot people also like that wait until after election. Just my own opinion, don't shoot me too hard. I belong to the 2nd group. Im against overpriced projects in non prime areas but ive never told anybody not to buy. I myself bought 2 condo's in Dec last year and am actively looking for my 5th property now. If uve read my earlier posts on other threads, ull know my strategies quite well. Facts cannot change and the fact is that 35,000 new condo's will be entering the market in 2015 alone with an equal number coming in 2016. Everybody is assuming these condo's will experience at least 15-20% increase in value and despite this there would be sufficient subsale buyers for these condos. If this was true, do tell me why many of the current projects which have obtained VP, are still experiencing 50% vacancy? Typical case is Solaris Dutamas, Mont Kiara. Despite having the popular Publika Mall below, the residences above are still generally empty. How is this so? If in 2013, there are no buyers, what then would be the condition in 2015/2016? Better? |

|

|

Mar 25 2013, 02:52 PM

|

|

Senior Member

1,801 posts Joined: Aug 2012 |

QUOTE(Nikmon @ Mar 25 2013, 01:00 PM) Nice work, we are at the top now. Congratulations. Correct me if I'm wrong on the following calculation....140% Debts/Disposable Household Income If Mr Z debt amt 300,000 Disposable Income = 300,000/1.4 = 214,285 (Annual income after Tax) Mr Z monthly income = 214,285/12 = 17,857 (after tax) 300,000 monthly payment est 1,500, I'll round off to 2,000 Mr Z income for other expenses after debt payment monthly = 17,857 - 2,000 = 15,857 I'm not into economic study or whatsoever, jus wonder anything wrong on my calculation?  And this does not included or concern on assets value too right? If the asset value 1,000,000 now? This post has been edited by AppreciativeMan: Mar 25 2013, 02:54 PM |

|

|

Mar 25 2013, 03:45 PM

|

Senior Member

1,331 posts Joined: Sep 2007 |

QUOTE(37 Exposures @ Mar 24 2013, 01:00 PM) Pointless....I bet 90% of Indonesians are rupiah millionaires... |

|

|

Mar 25 2013, 03:46 PM

|

|

Senior Member

1,331 posts Joined: Sep 2007 |

QUOTE(AppreciativeMan @ Mar 24 2013, 07:08 PM) I was neutral all the while.... However this weekend I think I'm leaning towards upside already.... LYF famous lawyer super confident correction or crash coming anytime, also jus plunge in to buy a prop at 664psf last week.... Who cares GE coming or not.... Or who says ppl waiting for GE over?..... Still back to square feet measurements....  I told you...it is never in my calculations when I buy props. |

|

|

Mar 25 2013, 03:50 PM

|

|

Senior Member

1,331 posts Joined: Sep 2007 |

QUOTE(cybermaster98 @ Mar 25 2013, 02:46 PM) Those who said property will slump in 2010 are not the same ppl today. U must learn to differentiate between the doomsday ppl and the real investors. Doomsday ppl will always speak negative bout the property any time and they are usually those who cannot afford high end properties themselves. While the real investors are those who know when and what properties to buy into anytime. You ask Appreciative Manlah why Mont Kiara some still empty...I belong to the 2nd group. Im against overpriced projects in non prime areas but ive never told anybody not to buy. I myself bought 2 condo's in Dec last year and am actively looking for my 5th property now. If uve read my earlier posts on other threads, ull know my strategies quite well. Facts cannot change and the fact is that 35,000 new condo's will be entering the market in 2015 alone with an equal number coming in 2016. Everybody is assuming these condo's will experience at least 15-20% increase in value and despite this there would be sufficient subsale buyers for these condos. If this was true, do tell me why many of the current projects which have obtained VP, are still experiencing 50% vacancy? Typical case is Solaris Dutamas, Mont Kiara. Despite having the popular Publika Mall below, the residences above are still generally empty. How is this so? If in 2013, there are no buyers, what then would be the condition in 2015/2016? Better? He is bullish about that place....can get 7% rental yield while buying middle of last year.... Me, I am just happy even if it is 5.3%. At least above inflation rate of 4%. Still need to park my cash somewhere else than equities, and sorry, gold is out for me... |

|

|

|

|

|

Mar 25 2013, 04:20 PM

|

|

Senior Member

1,864 posts Joined: Apr 2011 |

QUOTE(AppreciativeMan @ Mar 25 2013, 02:52 PM) Correct me if I'm wrong on the following calculation.... I think you are thinking all household debt are related to property debt, correct ? If you are referring to household debt, the usual bank guideline will be between 40%-60% of net income. Ie. If RM10k pm / RM120k pa net income, you can probably afford a property about RM1 mil. So the debt/income should be 8-10 times. What is 1.4 times ? Just chicken feet ratio 140% Debts/Disposable Household Income If Mr Z debt amt 300,000 Disposable Income = 300,000/1.4 = 214,285 (Annual income after Tax) Mr Z monthly income = 214,285/12 = 17,857 (after tax) 300,000 monthly payment est 1,500, I'll round off to 2,000 Mr Z income for other expenses after debt payment monthly = 17,857 - 2,000 = 15,857 I'm not into economic study or whatsoever, jus wonder anything wrong on my calculation? And this does not included or concern on assets value too right? If the asset value 1,000,000 now?  Especially like you said, value of properties is going up in long term. Especially like you said, value of properties is going up in long term. Unfortunately household debt is not property debt only. It includes car debt, credit card debt, personal loan (don't know if education loan included or not, but I think is is part of the household debt). In the reporting http://www.themalaysianinsider.com/malaysi...hold-debt-rises, the 4th last paragraph says "The bulk of the growth was contributed by the non-bank financial institution segment (NBFI) such as Bank Rakyat Sdn Bhd and Malaysia Building Society Bhd (MBSB), as concern grows over their lending to the lower-income segments." I think this is attributed to the personal loan to mainly government servant. If you are a government servant with RM4000 monthly salary, the bank will approve you RM200,000 of personal loan. These personal loan (and car and credit card loan) may be "non-productive loans", meaning it is consumption based instead of investment based (like property loan). So 140% is alarming if we compare to other countries. If the economy slows down, people start to lose their jobs, or interest rate increases, then we will feel the effect of servicing the debt. Suddenly, we need to use additional 20% of our income just to pay the installment. |

|

|

Mar 25 2013, 04:37 PM

|

|

Junior Member

139 posts Joined: Sep 2010 From: Kuala Lumpur |

QUOTE(AppreciativeMan @ Mar 25 2013, 02:52 PM) Correct me if I'm wrong on the following calculation.... I'm not sure what you are trying to get at but assuming a Debt of RM300k for Mr Z got you into trouble straight away. From that assumption, and working backwards, you derived income of RM17,857 pm. According to the Stats Dept, the mean Household Income in Malaysia in 2009 was only RM4,025 pm. A far cry from 17k.140% Debts/Disposable Household Income If Mr Z debt amt 300,000 Disposable Income = 300,000/1.4 = 214,285 (Annual income after Tax) Mr Z monthly income = 214,285/12 = 17,857 (after tax) 300,000 monthly payment est 1,500, I'll round off to 2,000 Mr Z income for other expenses after debt payment monthly = 17,857 - 2,000 = 15,857 I'm not into economic study or whatsoever, jus wonder anything wrong on my calculation? And this does not included or concern on assets value too right? If the asset value 1,000,000 now? |

|

|

Mar 25 2013, 04:50 PM

|

Senior Member

2,856 posts Joined: Jan 2010 |

QUOTE(tat3179 @ Mar 25 2013, 03:50 PM) You ask Appreciative Manlah why Mont Kiara some still empty... Im not promote mont kiara but have to clarify something, You have to understand the area, the development, the size and layout, can't fully rely on what people saying, or general data from the news. He is bullish about that place....can get 7% rental yield while buying middle of last year.... Me, I am just happy even if it is 5.3%. At least above inflation rate of 4%. Still need to park my cash somewhere else than equities, and sorry, gold is out for me... You have understand the demand from Jln Kiara, Jln Kiara 3, Kiara 5, kiaramas hillside, and Solaris area. The built-up, the rental price range etc, not all are doing bad, the Korean and Japanese prefer to live with their own community, some condo full of Korean and some are majority Japanese. For example; In kiaraville, you still can get gross 6.5% return with current subsales price. In Ceriaan, size between 1800-2200sf can still get decent return due to cheap entry price, and also opposite international school, whereas some other bigger size with asking above 9-10k rental not doing well. You need to understand your target market for your e-tiara, student market? Or others? Foreigner expat will give you less less less and lesser problem compare to student, I have expat tenant for my condo in Bukit Jalil, u know how difficult to get this expat, compare to Mont Kiara, they are everywhere, MK still their top choices bcos the 2 international school, the environment, the quality of neibourhood etc. You can't just concentrate on subang bcos you're staying there, as a investor, u need to study, survey and familiar other places in klang valley. |

|

|

Mar 25 2013, 04:55 PM

|

|

Senior Member

1,331 posts Joined: Sep 2007 |

QUOTE(zuiko407 @ Mar 25 2013, 04:50 PM) Im not promote mont kiara but have to clarify something, You have to understand the area, the development, the size and layout, can't fully rely on what people saying, or general data from the news. Fair enough, but I drove through there and Mont Kiara condos there appear like concrete mountains and contains a heck alot of units all competing for the expat market.You have understand the demand from Jln Kiara, Jln Kiara 3, Kiara 5, kiaramas hillside, and Solaris area. The built-up, the rental price range etc, not all are doing bad, the Korean and Japanese prefer to live with their own community, some condo full of Korean and some are majority Japanese. For example; In kiaraville, you still can get gross 6.5% return with current subsales price. In Ceriaan, size between 1800-2200sf can still get decent return due to cheap entry price, and also opposite international school, whereas some other bigger size with asking above 9-10k rental not doing well. You need to understand your target market for your e-tiara, student market? Or others? Foreigner expat will give you less less less and lesser problem compare to student, I have expat tenant for my condo in Bukit Jalil, u know how difficult to get this expat, compare to Mont Kiara, they are everywhere, MK still their top choices bcos the 2 international school, the environment, the quality of neibourhood etc. You can't just concentrate on subang bcos you're staying there, as a investor, u need to study, survey and familiar other places in klang valley. I mean they are not building low rises, but tall towers with hundreds and hundreds of units in one project. And there are many many projects there built already to me.... I mean, how many expats are there out there that is willing to rent all those units that there are out there...?  And the sub-sale prices ain't cheap man... |

|

|

Mar 25 2013, 05:01 PM

|

|

Senior Member

1,801 posts Joined: Aug 2012 |

QUOTE(EddyLB @ Mar 25 2013, 04:20 PM) I think you are thinking all household debt are related to property debt, correct ? If you are referring to household debt, the usual bank guideline will be between 40%-60% of net income. Ie. If RM10k pm / RM120k pa net income, you can probably afford a property about RM1 mil. So the debt/income should be 8-10 times. What is 1.4 times ? Just chicken feet ratio I'm aware debt inclusive of car loan, credit card outstanding and personal loan.... Tat is the reason why I rounded of the monthly installment to 2k.... Or I shld put it higher.... Lets say 4k monthly repayment in total.... Especially like you said, value of properties is going up in long term. Unfortunately household debt is not property debt only. It includes car debt, credit card debt, personal loan (don't know if education loan included or not, but I think is is part of the household debt). In the reporting http://www.themalaysianinsider.com/malaysi...hold-debt-rises, the 4th last paragraph says "The bulk of the growth was contributed by the non-bank financial institution segment (NBFI) such as Bank Rakyat Sdn Bhd and Malaysia Building Society Bhd (MBSB), as concern grows over their lending to the lower-income segments." I think this is attributed to the personal loan to mainly government servant. If you are a government servant with RM4000 monthly salary, the bank will approve you RM200,000 of personal loan. These personal loan (and car and credit card loan) may be "non-productive loans", meaning it is consumption based instead of investment based (like property loan). So 140% is alarming if we compare to other countries. If the economy slows down, people start to lose their jobs, or interest rate increases, then we will feel the effect of servicing the debt. Suddenly, we need to use additional 20% of our income just to pay the installment. Similarly working backwards, 17,857 - 4,000 = 13,857, there is still 13,857 balance for other expenditure.... Or I'll do another calculation, Mr Y Disposable income 5,000 mthly, basing on 140% ratio again what will be his debt amt? (5,000x12) x 1.4 = 84,000 (debt) I base on 6% interest, 15 yrs repayment, mthly repayment will be est 710 mthly, lets round off to 1,000 5,000 (income) - 1,000 (all debts) = 4,000 balance for other expenditure.... Any wrong on the following calculation again? Forget abt if there is any asset included in the debt.... This post has been edited by AppreciativeMan: Mar 25 2013, 05:04 PM |

|

|

Mar 25 2013, 05:11 PM

|

|

Senior Member

2,856 posts Joined: Jan 2010 |

QUOTE(tat3179 @ Mar 25 2013, 04:55 PM) Fair enough, but I drove through there and Mont Kiara condos there appear like concrete mountains and contains a heck alot of units all competing for the expat market. You need to do your homework for getting the answer of all your question.I mean they are not building low rises, but tall towers with hundreds and hundreds of units in one project. And there are many many projects there built already to me.... I mean, how many expats are there out there that is willing to rent all those units that there are out there...? And the sub-sale prices ain't cheap man... Without familiar with the place, the question will always on your head, u can also sell your existing unit, try to move here, I think you will love it, good for your children too |

|

|

Mar 25 2013, 05:14 PM

|

|

Senior Member

1,801 posts Joined: Aug 2012 |

QUOTE(tat3179 @ Mar 25 2013, 03:50 PM) You ask Appreciative Manlah why Mont Kiara some still empty... Aiyo.... Bullish is too strong a word to use ya.... And I hav never said tat.... We are not in court, don't try to put words into my mouth ya.... He is bullish about that place....can get 7% rental yield while buying middle of last year.... Me, I am just happy even if it is 5.3%. At least above inflation rate of 4%. Still need to park my cash somewhere else than equities, and sorry, gold is out for me... Thanks zuiko for explaining.... Frankly in general, MK large unit is tough to rent... But units as in 1-2 bedroom, u'll hav a larger choice of expat group. Believe it or not.... 1 bedroom is really high demand along Jln Kkiara like I says earlier.... Tat is why the yield can be high.... And there is still more in depth detail why I say I-zen is good.... And still a strong YES to MK for long term potential.... As I mention b4, the good quality condo will be in strong demand 10-20 yrs later.... Jus to add, more quality local are really moving into MK... My left and right neighbor are locals too, both 2 bedroom size unit..... This post has been edited by AppreciativeMan: Mar 25 2013, 05:23 PM |

|

Topic ClosedOptions

|

| Change to: |  0.0215sec 0.0215sec

0.60 0.60

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 2nd December 2025 - 05:30 PM |

Quote

Quote