May 6 2021, 04:00 PM

May 6 2021, 04:00 PM

QUOTE(roystevenung @ Dec 22 2020, 12:17 PM)

No, any extra premium paid, it will not go automatically into the Investment Unit Account (IUA).

It will go into a suspense account (floating) there until utilized.

If you intend to do top up into the policy underlying fund, you may do so via single top up or regular via prusaver 95% allocation rate.

My personal advice is to only do single top up, by monitoring yourself the trend of the fund.

Some agents may advise you to do regular top ups to do Dollar Cost Averaging, but personally for me its complete bull. Why? Is because if you do regularly, commission is earn, 3%!

Investing when the fund is at an all time high, good luck getting your money's worth. Just my 2 1/2 sense.

I was wondering why invest the funds when it is at an all time high..? isn't less units be bought?It will go into a suspense account (floating) there until utilized.

If you intend to do top up into the policy underlying fund, you may do so via single top up or regular via prusaver 95% allocation rate.

My personal advice is to only do single top up, by monitoring yourself the trend of the fund.

Some agents may advise you to do regular top ups to do Dollar Cost Averaging, but personally for me its complete bull. Why? Is because if you do regularly, commission is earn, 3%!

Investing when the fund is at an all time high, good luck getting your money's worth. Just my 2 1/2 sense.

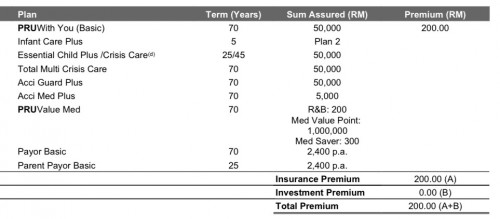

Quite headache to choose the funds..any recommendation?

This post has been edited by firee818: May 6 2021, 04:02 PM

Quote

Quote

0.0270sec

0.0270sec

0.49

0.49

6 queries

6 queries

GZIP Disabled

GZIP Disabled