Pm or asw2020 is better? My mum is gold member in pm n

she plans to transfer her money from asw2020 into pm.

Public Mutual v2, PB/Public series

Public Mutual v2, PB/Public series

|

|

Jun 9 2010, 07:48 AM Jun 9 2010, 07:48 AM

Return to original view | Post

#1

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

Pm or asw2020 is better? My mum is gold member in pm n

she plans to transfer her money from asw2020 into pm. |

|

|

|

|

|

Jun 27 2010, 02:24 PM

Return to original view | Post

#2

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

Hi unitholders, currently im helping my mother to plan our family funds. First of all, she invest in PM around 1996 and invest rm500 monthly until today for my sister. Which bring a total of 172k. She just blindly invest only. However, few weeks ago my mom opened another 1 account for me. Total 108k. I dont understand how the 5.5% charge works. Now my mum got around 120k in amanah saham wawasan 2020. So after ASW2020 pay out the interests, she plans to transfer all the money into PM. So here are the questions:

1. Should we put 120k into my sister's one? Based on my calculation, the returns for this year based on my sister account is 12%. Total amount invested rm61k+, and the return is 7k+(this is for 1 fund. got another fund i dont know the amount) Sorry im secondary school leaver so i dont know much about unit trust or mutual fund. Learning it now by the way. Because im solely looking at the return % only. Assuming invest 500k with minimum 8.5% return, can get RM42500 annually which is more than enough to bear my education fees + living expenses in college. 2. If put 120k into my account, will the return as high as in putting 120k into my sister account? 3. Is that worth to transfer all FD from other banks into PM? 4. I heard some people say PM is riskier than amanah saham. But from my POV, lately many rumors that government will bankrupt and bla bla due to corruptions. This make me trust PM more than ASW2020 but we still need to prepare for the worst case scenario. So if PM really going down, what to do? withdraw all the money? This post has been edited by mois: Jun 27 2010, 02:32 PM |

|

|

Jun 28 2010, 09:34 AM

Return to original view | Post

#3

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

hi gark, i just checked the datails.

1st one is regular saving fund 2nd one is ittikal fund Attached thumbnail(s)

|

|

|

Jun 28 2010, 06:05 PM

Return to original view | Post

#4

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(xuzen @ Jun 28 2010, 05:14 PM) Mois, i) What if i put 30k into X fund, then few days later i put 70k into X fund again? It charges 5.5% from 100k or 30k?i) 5.5 % works this way; let's say you invest RM 100,000 into X funds. Public Mutual will only invest using RM 100,000/1.055 = RM 94,786.73. The RM 5,213.27 will be deducted as initial charge. Half of this goes to the agent, and the other will go to Pub Mut i.e., RM 5,213.27/2 =RM 2,606.63 ii) No, it is not a good idea to put all the money from FD to PM. Maintain at least 6 months work of your average monthly expenditure in FD to cushion against emergency. iii) Only ASB has less risk simply because their buy/sell price is artificially maintained at RM 1.00/unit with regards to how market perform. I would put ASB more like a capital guarantee fund. Next a little comment on your PRSF (Public regular saving Fund) and PIttikal: PRSF is moderately performing, Pittikal is lousy performing. My comment is based on my computation of the funds using Jessen-Alpha Ratio and Treynor ratio. NB: I have access to the funds Beta, benchmark rtn and KLIBOR rtn. Better funds are PBGF (Public Bank Growth Fund) and PSF (Public Saving Fund) not Public Regular Saving Funds. Please note my comment are strictly based on 3 year average historical mathematical modeling. As always, past performance may not reflect the future performance.  ii) It is my mother extra FD. Around 200-300k left in FD  iii) After all since she invested in ASW2020 and not in ASB, so it is worth to transfer ASW2020(112k) into PM right? I found Public Growth Fund(PGF) instead of Public Bank Growth Fund. The PGF no doubt performing very well along with PSF. PGF last 3 years Distrubution yield(14.7%, 20.9%, 8.5%). Meanwhile PSF D.Y are (12.6%, 14.7%, 12.4%). Those are 2007-2008-2009. Still better than ASW2020 which offer less than 7%. |

|

|

Jul 7 2010, 12:32 PM

Return to original view | Post

#5

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

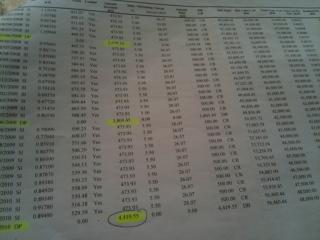

I would pick those

Public Saving Fund(PSF) Public Growth FUnd(PGF) Public Regular Saving Fund(PRSF) Public Ittikal Fund(P Ittikal) Public Equity Fund(PEF) Invested around 300k on those 5 Funds Few days ago i received Rm4419.55 cheque from Ittikal Fund. Total Cum. Cost is RM48000. Around 9% eh. Better than putting in FD and ASM. |

|

|

Jul 8 2010, 03:49 PM

Return to original view | Post

#6

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(N27 @ Jul 8 2010, 03:48 PM) Normally I would reinvest back dividend units instead of repurchase it. Keep it for a while until the NAV price shoot up back to the price before dividend is paid. How to reinvest back dividend? Just dont use the cheque? |

|

|

|

|

|

Jul 8 2010, 10:44 PM

Return to original view | Post

#7

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(Neonlight @ Jul 8 2010, 11:14 PM) Guys, I just checked for my dad fund Mind to share which funds are losing money?Total 6 fund, 2 lost money |

|

|

Jul 11 2010, 10:16 AM

Return to original view | Post

#8

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(wu ming @ Jul 11 2010, 10:50 AM) Just now teh tarik talk with my colleague. 30% return in how many years? Annually? Which fund is that? If the agent is a close friend of yours, u can ask them to check for u. Some agents are greedy. Agents get 2% commissions if i am not mistaken.One of my colleague (China man) claims that his friend made 30% from Public Mutual. Betulkah so easy? He said Public Mutual very good. Got good agents to monitor the funds. Yakah? |

|

|

Oct 1 2010, 09:45 AM

Return to original view | Post

#9

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(rkg38 @ Oct 1 2010, 10:13 AM) to all sifu here... 1 year? U cant. U need at least 3 years due to 5.5% service chargejs wanted to know, is there any fund suitable for 1yr investment?? cos i plan to save now, n withdraw at next year around this period... n will do monthly saving as well... any fund recommend? |

|

|

Nov 3 2010, 03:37 PM

Return to original view | Post

#10

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

Smallcap is open now? most of the time i heard it is full

|

|

|

Nov 4 2010, 05:56 PM

Return to original view | Post

#11

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

I just received a call from my agent. Equity fund has 12-13% return this year. Where to check the dividend pay out for each fund?

This post has been edited by mois: Nov 4 2010, 05:58 PM |

|

|

Nov 6 2010, 10:09 AM

Return to original view | Post

#12

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(jagz @ Nov 3 2010, 12:19 PM) Thank you Gark.. Actually PIttikal is good. I agree that I invested blindly. Not knowing what I was doing. Any place that you can recommend I can learn up. But for the current moment I am trying to see if what I have invested "makes sense" (which I believe has now  )... )...Thanks and sorry for all the noob questions Below are the funds that i invested. Some are more than a decade already. PIttikal Public Equity Public Growth Fund Public Regular Saving Fund Public Saving These 5 funds are quite stable from my experiences. Gark, any comments? |

|

|

Nov 6 2010, 12:21 PM

Return to original view | Post

#13

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(gark @ Nov 6 2010, 11:39 AM) Nobody does anymore research nowadays. Hmmph... Actually i park my parent money inside those funds since 1996. Some are newly invested. But as long higher than asw2020 is ok. Because mine full and the return for asw2020 less than 7% lol. All the funds you mentioned are all in the same category and all of them roughly hold the same stocks in every fund. Why would you buy a bunch of similar funds, hence do not have diversification? You should diversify some of your funds out of Malaysia and hold some bond funds for diversification. Of the funds above only PIttikal and Public Savings are the laggards, compared to the rest. By the way all of the funds above perform lower/around the benchmark for last 1 year.  , but for 5 years they were quite good. , but for 5 years they were quite good.Anyway I am sure, others have their own opinions.  Overseas funds perform better? The returns around how much? Above 8% is ok for me. Last time my mom invest a little on public bond. But progress so slow then switch it to another fund. And holding the same category of funds that have steady return is not bad.  This post has been edited by mois: Nov 6 2010, 12:29 PM |

|

|

|

|

|

Nov 6 2010, 05:54 PM

Return to original view | Post

#14

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(buylowsellhigh @ Nov 6 2010, 03:18 PM) Added on November 6, 2010, 2:27 pm i agree with gark. here is my 2 cents. at the end of the day, if you are happy with the return, then do nothing. if you want to be more agressive, then select more agressive funds. But if you go for agressive but dont switch, your potential loss is also agressive. which then brings us to the question of how comfortable are you switching or do you have someone to help you.<---my problem And during 2008, the advanced investors will switch from equity fund to bond fund? since bond fund is low risk profile. I read your article regarding the switching thing. It looks simple when u draw the table for Equity vs bond. But how to predict whether the NAV is going down or up? Because it is better to switch to bond fund before the NAV of the equity at the lowest right? And then switch back to equity fund during the 'recovery mode'. Problem is im not really clear when is the best time to switch.  This post has been edited by mois: Nov 6 2010, 06:43 PM |

|

|

Nov 10 2010, 08:46 AM

Return to original view | Post

#15

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

Recently China Select and China Ittikal shooting up pretty fast. Anyone invest in these two funds?

|

|

|

Nov 10 2010, 09:59 AM

Return to original view | Post

#16

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(gark @ Nov 10 2010, 10:10 AM) Not really performing to good long term compared to benchmark. So gave it a miss. Generally PM funds have not proven themselves for oversea fund performance (maybe lack of experience?). Yea this fund is not really good for long term and perform below benchmark. But lately it bounces back strongly. what i plan to do is switch few k units since the market is good now and the NAV is shooting up. If the fund is falling, i will switch back when it falls to the NAV i bought it. This one i will monitor often. Switching is free though. So i dont count the 5.5%. What do u think? Should stay with what i have now or go 'explore' high volatile fund? China Select - performing way below benchmark China Ittikal - performing slightly below benchmark PS: I use small volume only. Probably RM5-7k. Otherwise i will be in deep trouble if my plans dont work out. . And of course i wont decide so fast. Need opinions from pros/agents.This post has been edited by mois: Nov 10 2010, 10:03 AM |

|

|

Nov 15 2010, 01:52 PM

Return to original view | Post

#17

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

Most funds are dropping since a week ago. My agent told me not to do so much switching. Weird.

|

|

|

Nov 30 2010, 11:32 PM

Return to original view | Post

#18

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(howszat @ Nov 30 2010, 11:51 PM) Yeah no service charge on reinvestments. There is practically no difference in the total value/cost of the investment before and after dividend. More units, more money I did forget one thing though. After dividend, you have more units. It makes people happy because they have more units. It doesn't matter that they don't actually have more money.  how to more money if less units? unless the NAV stay the same. how to more money if less units? unless the NAV stay the same. |

|

|

Nov 30 2010, 11:43 PM

Return to original view | Post

#19

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(David83 @ Dec 1 2010, 12:34 AM) Didn't I say earlier that your NAV will be adjusted down once distribution is cleared. If the next day NAV slides down, meaning what you're in loss. I know it slides down after DR. But if the NAV bounce back just like it was before the distribution, still untung right?Before the distribution, the "value" is still retained the same; provided that distribution is reinvested and NAV does not change. 1000units Before distribution, NAV RM1. After DR, RM0.8. Assuming i have 1200units at RM0.8 Wait 2-3months(if market steady lah) The nav back to RM1. so now i have 1200units x RM1 = RM1200. Correct? |

|

|

Dec 1 2010, 12:03 AM

Return to original view | Post

#20

|

|

Senior Member

3,626 posts Joined: Nov 2007 From: Hornbill land |

QUOTE(David83 @ Dec 1 2010, 12:49 AM) You have the point - optimism way of looking into it but NAV movement can be the other way as well. Let's not talk about the future since we all don't own a crystal ball. ok i get it. Do u guys choose to reinvest or pay out cheque? And do u guys switch over to bond fund if NAV drop over 5-7%? I dont want like last time my agent did nothing during 2008 crisis What I would like to stress of the "value" before and after distribution.  |

|

Topic ClosedOptions

|

| Change to: |  0.7264sec 0.7264sec

1.01 1.01

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 9th December 2025 - 03:00 PM |

Quote

Quote